Scientific Due Diligence for Brilaroxazine: Reviva Pharmaceuticals (RVPH)

Can One Phase 3 Trial Unlock a Billion-Dollar Drug?

Executive Summary

The Hook:

Imagine Abilify (aripiprazole)—one of the best-selling antipsychotics of all time—but without the restlessness (akathisia) or metabolic baggage. That is the pitch for Brilaroxazine (RP5063). It’s touted as a cleaned-up serotonin-dopamine modulator that aims to be the new Standard of Care (SoC) drug for schizophrenia: potent enough to stop psychosis, but gentle enough to avoid side-effects that have substantially limited patient compliance.

The Bull Case:

Brilaroxazine is a clinically validated New Chemical Entity (NCE) that hit its primary endpoints in a global Phase 3 trial (RECOVER-1) with solid effect sizes and a seemingly clean safety profile. If the FDA accepts a single Phase 3 trial for NDA submission (a regulatory gamble Reviva is actively taking), RVPH is sitting on a de-risked asset worth multiples of its current micro-cap valuation. It is a prime bolt-on acquisition target for a mid-to-large-sized Pharma looking to refresh its CNS franchise.

The Bear Case:

The schizophrenia market is a graveyard of me-too drugs. Brilaroxazine is entering a ring dominated by cheap generics and the new heavyweight champion, KarXT (Cobenfy), which has a novel mechanism (muscarinic). Furthermore, Reviva is playing a dangerous game of regulatory chicken. They are betting the house that the FDA will accept one Phase 3 trial. If the FDA demands a second Phase 3 study (RECOVER-2), Reviva likely does not have the cash to run it. The stock could effectively go to zero on that news.

Bottom Line:

Speculative Buy. The science works, but the balance sheet is broken. This is a binary bet on a pre-NDA meeting with the FDA (which is either happening soon or has already happened, the latter being less likely IMO). If the FDA gives positive guidance for submitting an NDA based on current data, this is a multi-bagger. If they require a second trial, it’s a dilution disaster.

Catalyst Calendar & Financial Runway

Upcoming Catalysts:

Q4 2025 (IMMINENT): Pre-NDA Meeting with FDA. This is the make or break event. Management will ask if their single Phase 3 trial + Open Label Extension (OLE) data is sufficient for approval. A “Yes” sends the stock soaring; a “No” (requiring RECOVER-2) crushes it [Source: 10-Q, pg. 30].

Q4 2025 to Q1 2026: Minutes/Feedback from FDA meeting. There is a chance Reviva presents the virdict from the meeting during their annual shareholder meeting on December 18, 2025.

Q2 2026: Targeted NDA Submission (contingent on favorable pre-NDA meeting).

The Dilution Gap: CRITICAL RED FLAG

Cash on Hand: ~$13.2M (as of Sept 30, 2025) [Source: 10-Q, pg. 3].

Burn Rate: ~$4M per quarter (Net loss was ~$4M in Q3 2025) [Source: 10-Q, pg. 4].

Runway: Management claims cash lasts into Q2 2026 [Source: 10-Q, pg. 9].

The Reality: They are running on fumes. Even if the FDA says “yes,” they need cash to file the NDA and prep commercialization. If the FDA says “no,” they need $50M+ for a new trial. Expect a reverse split and/or capital raise (dilution) imminently, likely timed around any positive news from the FDA meeting.

Insiders & Institutions:

Insiders: CEO Laxminarayan Bhat appears to own ~2%, showing skin in the game but not controlling interest. Recent activity shows some routine sales, likely for tax/options.

Institutions: Vanguard and BlackRock appear to have small positions, but this appears to be largely a retail/speculator-owned stock.

The Science: Mechanism & Chemistry

NCE. Brilaroxazine is a distinct chemical entity (a phenylpiperazine derivative), though it is highly structurally similar with the aripiprazole/brexpiprazole family.

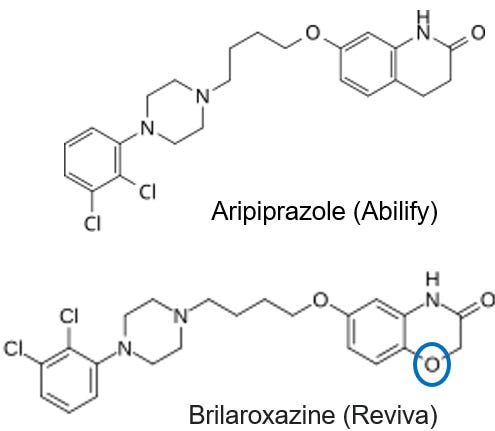

Chemical Structure

Brilaroxazine is structurally very similar to Aripiprazole (Abilify), which is one of the current standards of care for schizophrenia. Comparing the structures below, you can see that the heterocyclic group of Brilaroxazine has an oxygen atom instead of a carbon atom. Even this minor structural change can have huge impacts in efficacy, tolerability, etc., as has been demonstrated by Reviva to date.

Mechanism Validation:

Target: Partial agonist at Dopamine D2/D3/D4 and Serotonin 5-HT1A; antagonist at 5-HT2A/2B/7.

The Twist: The high affinity for 5-HT7 and 5-HT2B is the differentiator. 5-HT7 modulation is linked to pro-cognitive effects (fixing brain fog). 5-HT2B antagonism is the secret sauce, including for their secondary indications in Pulmonary Arterial Hypertension (PAH) and Fibrosis (IPF), where serotonin drives lung scarring [Source: Investor Presentation, pg. 28].

Validation: The dopamine-serotonin modulation mechanism is thoroughly validated by blockbuster drugs (Abilify, Vraylar, Rexulti). The biological risk here is near zero; we know this mechanism treats psychosis.

Clinical Data

Efficacy (RECOVER-1 Phase 3 Trial):

The Headline: 50mg dose achieved a 10.1-point reduction in PANSS Total Score vs. Placebo (p<0.001) [Source: Investor Presentation, pg. 8].

Reality Check: The effect size (Cohen’s d = 0.6) is solid. For context, most antipsychotics hover around 0.4-0.5. This is a robust signal.

Differentiation: Reviva reports improvements in Negative Symptoms (social withdrawal, apathy) and Cognition. While Reviva showed statistical significance here, we can be skeptical. Every antipsychotic developer claims “negative symptom efficacy,” but few deliver in the real world. The data looks better than placebo, but head-to-head against Vraylar (cariprazine) would be the real test.

The P-Hacking Check:

The 15mg Dose: The 15mg dose was numerically superior but the p-values were mixed on secondary endpoints. The 50mg dose is clearly the therapeutic winner. This isn’t p-hacking; it’s a clear dose-response, which is actually a good sign of pharmacological activity.

Safety/Tolerability:

This is the real differentiator.

Weight Gain: Only ~1.3kg gain over 1 year (50mg). This is excellent compared to drugs like Olanzapine (can be +5-10kg).

Metabolic: No significant changes in glucose or lipids [Source: Investor Presentation, pg. 19].

Motor Side Effects: Akathisia (the “crawling out of your skin” feeling) was <1% for the 50mg dose. For comparison, Abilify/Latuda can have rates of 10-15%+. This is a commercially viable differentiator. Doctors hate prescribing drugs that make patients agitated.

Data Integrity:

The Risk: They are relying on one pivotal trial (RECOVER-1) and an Open-Label Extension (OLE). The standard FDA requirement is two pivotal trials.

The Gamble: Reviva’s position will be that the data is sufficiently robust (p<0.001) and the unmet need (safety) is sufficiently high, that one trial should suffice. This happened with Nuplazid (pimavanserin), but it’s rare. Reviva will likely also try to leverage the data from their open-label study as an additional data point.

The One-Trial Regulatory Play: While CNS approval typically requires two Phase 3 trials, the FDA has statutory authority (via FDAMA 1997) to approve drugs based on a single adequate and well-controlled trial if accompanied by “confirmatory evidence”.

Example Precedent: Nuplazid (pimavanserin) was approved for Parkinson’s Disease Psychosis on the basis of a single pivotal Phase 3 trial.

Reviva’s Case: Brilaroxazine’s RECOVER-1 data yielded a highly robust p-value (p<0.001 for the 50mg dose), which far exceeds the standard p<0.05 threshold, potentially satisfying the FDA’s requirement for “robust” statistical persuasiveness in single-trial scenarios.

Confirmatory Evidence: Reviva will argue that their “confirmatory evidence” package is substantial, including the successful Phase 2 (REFRESH) study, 12-month Open-Label Extension (OLE) safety data, and mechanistic validation from other approved serotonin-dopamine modulators (like Abilify and Vraylar).

Intellectual Property & The Moat

Ownership & Patents:

Wholly Owned: No messy licensing fees to a university or big pharma partner identified.

Patent Life: Composition of matter in the US until at least 2030, with extensions likely pushing exclusivity to 2035. Method of treatment patents should extend coverage into at least the late 2030s. This is a relatively shorter runway, which may lower (M&A) valuation, but it could still provide sufficient time for a potential acquirer to recoup their investment [Source: 10-Q, pg. 28].

New IP: Reviva recently secured a European patent for Pulmonary Fibrosis (Nov 2025), expanding the story beyond schizophrenia [Source: Press Release].

The Competitive Landscape:

The Gorilla: KarXT (Cobenfy). Bristol Myers Squibb bought Karuna for $14B for it’s assets. It works on muscarinic receptors (no dopamine blockade), meaning zero motor side effects and weight loss. It is the new Standard of Care.

The Generics: Aripiprazole (Abilify) is generic and costs pennies.

The Niche: Brilaroxazine’s play is the safe switch. If KarXT fails a patient (GI side effects) or Generics cause akathisia, Brilaroxazine is the logical next step. It doesn’t have to beat KarXT; it just needs to be the best dopamine modulator.

Pipeline

While Schizophrenia is the main event, the Bull Case also relies on Brilaroxazine being a pipeline in a pill—a single molecule with multiple (6 other) potential indications.

The Hidden Gem: Respiratory & Fibrosis (PAH & IPF):

The Science: Most antipsychotics effects are in the brain, but Brilaroxazine’s potent antagonism of the 5-HT2B receptor gives it a unique potential application in the lungs. 5-HT2B overexpression drives fibrosis (scarring) and vasoconstriction.

The Validation: The FDA has already granted Orphan Drug Designation for both Pulmonary Arterial Hypertension (PAH) and Idiopathic Pulmonary Fibrosis (IPF).

Why it Matters: This isn’t just lifecycle management; it opens the door to entirely different (and lucrative) orphan disease markets ($12B+ opportunity). The molecule still has intrinsic value as a fibrosis asset.

Standard Lifecycle Management (Bipolar, MDD, ADHD):

Reviva has completed Phase 1 studies for Bipolar Disorder, Major Depressive Disorder, and ADHD. This is standard operating procedure for this drug class (similar to how Vraylar expanded from Schizophrenia to Bipolar/MDD), but don’t price this in yet. These trials are expensive and currently unfunded.

The Next Bat at the Plate: RP1208:

This is their preclinical NCE, a Triple Reuptake Inhibitor (serotonin, norepinephrine, dopamine) targeting Depression and—more interestingly—Obesity.

The Reality Check: While triple inhibitors are scientifically potent, this asset is sitting in preclinical limbo. It is “eady for IND-enabling studies, but without cash, it’s just a structure on a slide.

Pipeline Summary: The PAH/IPF data appears to be genuinely differentiating science that separates Reviva from generic antipsychotic developers. However, investors must be realistic: Reviva does not have the cash to run these trials. This pipeline exists primarily to sweeten the pot for a potential acquirer who does have the budget to unlock these indications.

The Verdict

Scientific Conviction: High (9/10).

On it’s face, the molecule appears to be a better mousetrap. It seems to bind to the “right” receptors, the Phase 3 data looks unequivocal, and the safety profile appears to address the biggest complaints patients have with current meds.

Commercial Viability: Medium (5/10).

Even if approved, launching a psychiatry drug requires a massive sales force. Reviva cannot do this alone. They very likely must partner or be acquired. Without a partner, they are a commercial science project.

The M&A Appeal: High.

A safe, effective, Phase 3-finished CNS asset with patents into at least the late 2030s. This is prime meat for a company like AbbVie, Otsuka, or Lundbeck. The current market cap (~$76M) is a rounding error for them. Reviva also has a pipeline that could add a sweetener to for a potential partner/acquirer.

I highly suggest reading the M&A analysis by M&A Hunter here: https://substack.com/@maandhunter/p-179988337

Trader Profile: Binary Event Gambler.

If you own this, you are holding a lottery ticket for the FDA meeting outcome.

Final Verdict: WATCH LIST (Hold and accumulate on weakness if you have risk tolerance).

Hold if your conviction is strong that the FDA will give positive guidance during the pre-NDA meeting.

Buy if the stock dips on financing news, provided the FDA meeting tone remains constructive.

Exit strategy: IMMEDIATELY sell if FDA guidance from pre-NDA meeting is negative; or sell into the spike on positive pre-NDA meeting news; consider holding a certain position percentage going into potential FDA acceptance of the NDA submission in Q2 2026.

Disclaimer: This is not financial advice. I am a chemist and an analyst, not your wealth manager. Biopharma stocks are volatile and can go to zero. Do your own due diligence.

This report is strictly for informational and educational purposes. It does not constitute investment advice, financial planning, or a recommendation to buy, sell, or hold any securities. I analyze molecules and mechanisms, not portfolios. All investment decisions should be made in consultation with a qualified financial advisor and based on your own risk tolerance and due diligence.

The scientific analysis contained herein is intended solely for investment due diligence. It should not be interpreted as medical guidance, diagnosis, or a recommendation for treatment. Do not use this report to self-medicate or alter your health regimen; always consult a licensed healthcare provider.

At the time of writing, the author holds a long position in Reviva Pharmaceuticals (RVPH) consisting of both common stock and call options.

Biotech investing is a high-risk, high-volatility asset class. Clinical trials fail, the FDA is unpredictable, and companies run out of cash. Past scientific validation does not guarantee future clinical success or regulatory approval. Invest only what you can afford to lose.

For informational and educational purposes only — not investment advice. The author's position (if any) is as stated in the original article. Always verify against primary sources and do your own due diligence.