Milestone Pharmaceuticals (MIST): Scientific Due Diligence for CARDAMYST (etripamil) and Pipeline

FDA Approved, Funded to Launch, and Protected until 2042: A deep dive into etripamil’s chemistry and commercial moat.

Executive Summary

The Hook:

Milestone Pharmaceuticals has effectively taken a hospital-grade procedure—converting a racing heart (PSVT) back to normal rhythm—and put it in a nasal spray. For 30 years, the gold standard for PSVT has been IV Adenosine, a drug known for two things: working instantly, and causing a terrifying sensation often described by patients as a sense of impending doom. CARDAMYST (etripamil) offers a Calcium Channel Blocker (CCB) mechanism that patients can self-administer without the hospital trip and without the doom.

The Bull Case:

With the FDA approval secured as of December 12, 2025, MIST transitions from a binary-risk biotech to a commercial execution story. The addressable market is respectable (~2 million Americans with PSVT), and the competition is largely nonexistent or inconvenient (ER visits/off-label generic pills). If they capture even a fraction of the frequent-flyer PSVT patients, this is a blockbuster in a niche device.

The Bear Case:

Commercial launches for acute on-demand therapies are notoriously slow burns. Patients must carry the device to use it. If the drug is priced too high, insurers will force patients to try vagal maneuvers (holding breath/bearing down) or cheap generic pills first. Furthermore, the placebo response in their trials was high (~31%), meaning 1 in 3 patients might convert to normal rhythm just by sitting down and waiting, potentially eroding the perceived value of the drug.

Bottom Line:

Buy. The science works, the regulatory risk is off the table for PSVT, and the balance sheet just got a massive non-dilutive injection. The risk now shifts entirely to commercial adoption and pipeline follow through. This is a “Buy” for value-oriented biotech investors, but patience is required for the launch ramp and pipeline development.

Catalyst Calendar & Financial Runway

Upcoming Catalysts:

Q1 2026. Commercial Launch of CARDAMYST in retail pharmacies [Source: 8-K (Dec. 15, 2025), pg. 32].

2026 (TBD): Initiation of Phase 3 trial for the second indication: Atrial Fibrillation with Rapid Ventricular Rate (AFib-RVR). Note: Enrollment was paused pending the PSVT approval [Source: Corporate Slides, pg. 28].

Quarterly Earnings: Watch for “New-to-Brand Prescriptions (NBRx)” metrics post-launch.

Phase 3 Initiation for AFib-RVR (2026): With the PSVT approval secured, the company is now poised to enter a pivotal Phase 3 program for its second indication: Atrial Fibrillation with Rapid Ventricular Rate (AFib-RVR). This study was previously set up but paused to conserve capital during the NDA review. It targets a patient population potentially larger than PSVT and utilizes a streamlined Supplemental New Drug Application (sNDA) regulatory pathway [Source: 8-K (Dec. 15, 2025), pg. 33].

The Dilution Gap:

Cash Position (Sept 30, 2025): $82.6M. [Source: 10-Q, pg. 5].

The Approval Windfall: The FDA approval on Dec 12, 2025, triggered a $75 million royalty payment from RTW Investments [Source: 10-Q, pg. 18].

Total Pro-Forma Liquidity: ~$157M.

Burn Rate: Operating loss was ~$11.8M in Q3 2025. Commercial expenses spiked 142% in Q3 as they prepped for launch [Source: 10-Q, pg. 6].

Verdict: No immediate dilution gap expected. The RTW payment is a lifeline that bridges them well into the commercial launch. They are well-capitalized to execute without an immediate secondary offering.

Insiders & Institutions:

Recent Activity: CEO Joseph Oliveto and CFO Amit Hasija adopted Rule 10b5-1 trading plans in Sept 2025. This is standard hygiene but indicates planned liquidity events now that the stock is de-risked [Source: 10-Q, pg. 42].

The Science: Mechanism & Chemistry

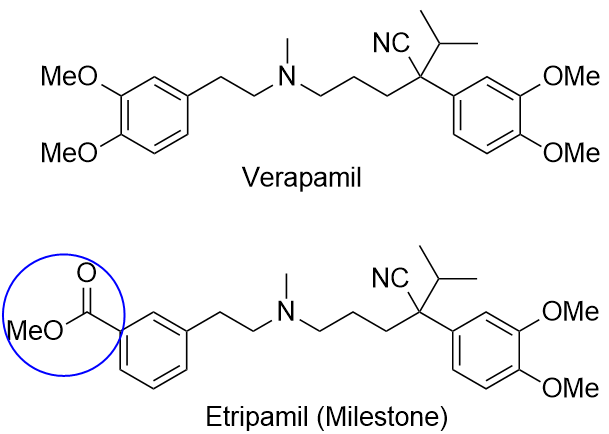

Chemical Structure

Etripamil is a “soft drug” analog of verapamil (a classic Calcium Channel Blocker). Milestone modified the chemistry to include a metabolically labile ester moiety (see below).

Mechanism and Validation:

Etripamil acts like a potent heart drug for about 30 minutes, then blood esterases rapidly chop it up into inactive byproducts. This “fast-on, fast-off” profile is what makes it safe to sniff. Classic oral CCBs stay in the system too long, causing prolonged low blood pressure (hypotension)—a dealbreaker for acute self-administration.

Target: L-type Calcium Channels in the AV Node.

Validation: High. This is arguably the most validated mechanism in cardiology – CCBs have been used for decades. The risk was never “does the biology work?” It was “can we dose it high enough to work fast without crashing the patient’s blood pressure?” The nasal route bypasses first-pass metabolism, hitting the heart quickly.

Manufacturing/CMC:

Past Trauma: The March 2025 Complete Response Letter (CRL) was entirely due to CMC issues (Nitrosamine impurities and a facility inspection) [Source: Investor Presentation, pg. 31].

Resolution: The FDA accepted their fix and granted approval. While CMC was a risk, the approval confirms the nitrosamine levels are now within acceptable limits and the facility passed inspection [Source: Dec. 2025 8K, pg. 32].

Clinical Data

Efficacy: RAPID Trial (Phase 3):

The Headline: 64.3% of CARDAMYST patients converted to normal rhythm within 30 minutes vs. 31.2% on placebo. HR 2.62, p<0.001 [Source: Dec. 2025 8K, pg. 38].

The Reality Check:

Effect Size: The drug doubles your chance of converting compared to doing nothing (placebo).

Speed: Median time to conversion was 17 minutes for the drug vs. 54 minutes for placebo [Source: Dec. 2025 8K, pg. 33].

The Placebo Problem: A 31% placebo cure rate is high. This is because PSVT can self-terminate with rest or vagal maneuvers (which patients likely tried).

Clinical Value: While 1 in 3 placebo patients got better, they took nearly an hour. The drug works 3x faster. In a panic attack/heart episode, 40 minutes of time savings is clinically meaningful.

Safety/Tolerability:

Heart Block: Zero reported cases of Mobitz II or 3rd-degree AV block. This is the

”widowmaker” risk with CCBs, and it appears absent here due to the short half-life – huge potential value [Source: Dec. 2025 8K, pg. 10].Hypotension: Only 0.4% experienced low blood pressure within 24 hours [Source: Dec. 2025 8K, pg. 10].

The Nuisance AE: 25% of patients had adverse events, mostly Nasal Discomfort and Congestion. This is the trade-off. It burns your nose, but it fixes your heart. Most patients will take that deal [Source: Dec. 2025 8K, pg. 10].

Data Integrity:

Design: Randomized, Double-Blind, Placebo-Controlled (RAPID Trial).

Sample Size: N=706 enrolled. This is a robust dataset for a rare/episodic condition [Source: 10Q, pg. 23].

Intellectual Property & The Moat

Ownership & Patents:

Ownership: Milestone owns the asset. There are no “poison pill” licensing structures visible in the 10-Q that would deter an acquirer.

China Rights: Licensed to Corxel (formerly Ji Xing) for Greater China. This provides non-dilutive milestone revenue potential but limits the global upside slightly. [Source: 10-Q, pg. 26].

Patent Life:

Expiry: Patents appear to run until 2042. A recently issued U.S. patent covers the “repeat dose” regimen (the ability to take a second spray if the first fails). This IP should also cover dosing regimens for pipeline indications, such as Afib RVR [Source: Dec. 2025 8K, pg. 15].

Analysis: 2042 should be acceptable for pharma. Generic entry should be decades away.

The Competitive Landscape:

Direct Competitors: “No anticipated branded competition” [Source: Dec. 2025 8K, pg. 18].

Indirect Competitors:

Vagal Maneuvers: Free, but low efficacy (~20-30%).

“Pill-in-Pocket” (Oral Diltiazem/Verapamil): Takes 45-60+ minutes to work.

Ablation: Curative but invasive. Only ~15% of eligible patients choose it due to fear/cost [Source: Investor Presentation, pg. 7].

IV Adenosine & The ER Visit: While not a direct commercial rival in the pharmacy, the status quo is the biggest hurdle. The current standard of care requires an IV infusion in a hospital setting , a process described as “burdensome” and “stressful” for patients. With PSVT management costing the healthcare system “at least $5 billion” annually, CARDAMYST’s main battle is convincing physicians to trade the certainty of a hospital procedure for the convenience of patient self-management.

Differentiation: CARDAMYST sets itself to be the best option that fills the gap between “holding your breath” and “going to the ER.”

Pipeline

While CARDAMYST for PSVT is the immediate revenue driver, the bull case for Milestone relies on leveraging etripamil into larger indications. The company is effectively a single-asset story, but that single asset has pipeline-in-a-product potential.

The Big Prize: Atrial Fibrillation with Rapid Ventricular Rate (AFib-RVR):

The Opportunity: AFib-RVR affects a patient population estimated to be 2-3x larger than PSVT. Like PSVT, these patients often flood emergency rooms simply to get their heart rate lowered.

Status: Phase 3 Ready.

Data So Far (ReVeRA Phase 2): The Phase 2 ReVeRA trial met its primary endpoint with high statistical significance (p < 0.0001). Patients treated with etripamil saw a mean ventricular rate reduction of ~30 bpm compared to placebo.

Regulatory Path: Milestone has already aligned with the FDA on a Phase 3 registrational program. This will utilize a Supplemental New Drug Application (sNDA) pathway, meaning they can leverage the massive safety database from the PSVT program, saving time and money. Enrollment was paused to conserve cash during the PSVT approval delay but is expected to restart now that the CRL is resolved.

Pediatric PSVT

Status: Phase 2 Ongoing.

The Angle: While a smaller market commercially, expanding the label to pediatrics provides regulatory goodwill and extends the patent/exclusivity lifecycle.

The Risk: Single-Asset Concentration

Investor Note: Milestone currently has no disclosed clinical assets outside of etripamil. If the commercial launch for PSVT fails or safety signals emerge in the broader population, there is no “backup” molecule to pivot to. The investment thesis is entirely tethered to the commercial success of this specific chemical entity.

The Verdict

Scientific Conviction: High.

Validated mechanism, clever “soft drug” chemistry, P<0.001 Phase 3 data.

Commercial Viability: Medium.

Launching a “carry-with-you” device requires changing patient behavior. Pricing will be key to avoiding payer “step edits.”

The M&A Appeal: High.

This is a bolt-on dream for a mid-cap pharma with a cardiology sales force. The heavy lifting (R&D, FDA) is done.

Trader Profile:

Long-term Value Holders: The approval de-risks the asset. The royalty cash bridges the gap. The patent life (2042) ensures long-tail cash flow.

Avoid: If you are looking for a 10x in a month. The “approval pop” appears to have already happened/been priced in. This is now a slow execution climb.

Final Verdict: BUY. The approval + the $75M cash infusion creates a very favorable risk/reward profile. The science is real, the clinical benefit (speed + self-reliance) is tangible, and the moat is deep. The biggest risk is a sluggish launch curve, but the cash buffer buys them time to get it right.

Disclaimer: This is not financial advice. I am a chemist and an analyst, not your wealth manager. Biopharma stocks are volatile and can go to zero. Do your own due diligence.

This report is for informational and educational purposes only. It does not constitute investment advice, a recommendation to buy or sell any securities, or an offer to provide investment advisory services..

The scientific analysis presented here regarding etripamil and cardiovascular conditions is for investment due diligence purposes only and should not be interpreted as medical guidance.

At the time of writing, the author holds a long position in Milestone Pharmaceuticals (MIST) consisting of common stock.

Biotech investing is volatile. Past scientific validation does not guarantee commercial success. Regulatory approvals can be followed by commercial failures. Invest at your own risk.

For informational and educational purposes only — not investment advice. The author's position (if any) is as stated in the original article. Always verify against primary sources and do your own due diligence.