CervoMed (CRVO): Scientific Due Diligence for Neflamapimod

The ‘Bad Batch’ Theory, Synaptic Rescue, and the Race Against Dilution

Executive Summary

The Hook:

In biotech, “the dog ate my homework” is a classic excuse for failed trials. CervoMed offers a sophisticated variation: “The pills aged poorly.” Their Phase 2b trial for Dementia with Lewy Bodies (DLB) technically failed its primary endpoint. However, the company argues this wasn’t a biological failure, but a chemical one — specifically, that the drug capsules used in the first phase (”Batch A”) underwent a polymorphic change that killed bioavailability. When they switched to fresh capsules (”Batch B”) in the extension phase, the drug seemingly worked.

The Bull Case:

If the “Batch” theory is chemically sound (and it is plausible), CervoMed is sitting on a de-risked asset that just needs a manufacturing fix to succeed in Phase 3. They are targeting pure DLB — patients without Alzheimer’s co-pathology — creating a homogeneous population that can maximize the signal of their drug, neflamapimod.

The Bear Case:

You are betting on a post-hoc subgroup analysis of an open-label extension study. If the “Batch B” performance was just a placebo effect or selection bias (healthier patients staying in the trial), the Phase 3 will fail catastrophically. Meanwhile, the cash runway is terrifyingly short.

Bottom Line:

CervoMed is a high-risk, binary bet on manufacturing chemistry, not just biology. They have a scientifically reasonable hypothesis for their failure, but they need to raise capital immediately to prove it in Phase 3.

Catalyst Calendar & Financial Runway

Upcoming Catalysts:

Early 2026: Protocol finalization with global regulators.

2H 2026: Initiation of the Phase 3 pivotal trial in DLB (300 patients).

The Dilution Gap: CRITICAL RED FLAG.

Cash on Hand: ~$27.3M (as of Sept 30, 2025).

Burn Rate: ~$8M per quarter (Loss from operations).

Runway: Less than 12 months. The company explicitly states “substantial doubt” about going concern status.

The Gap: They plan to initiate Phase 3 in 2H 2026. Their cash runs out before the trial even starts.

Implication: A partnership or capital raise is imminent. Expect one of these before any major data readout.

The Science: Mechanism & Chemistry Summary

Neflamapimod is not a new molecule. It is VX-745, originally discovered by Vertex Pharmaceuticals. It’s a p38 alpha kinase inhibitor. Vertex dropped it; CervoMed (formerly EIP Pharma) repurposed it for CNS. This means the composition-of-matter patents on the molecule itself are likely aged-out, forcing reliance on formulation/polymorph patents.

Mechanism Validation:

The Logic: P38 alpha kinase is a stress-response enzyme. In the brain, its chronic activation drives neuroinflammation and synaptic dysfunction (neurons stop talking to each other). Inhibiting it should help.

The Trap: P38 inhibitors have a notorious history of toxicity (liver enzymes, skin reactions) and failing in rheumatoid arthritis due to tachyphylaxis (the body adapts and the drug stops working).

CervoMed’s Twist: They argue that in pure DLB, the primary driver is reversible synaptic dysfunction in the basal forebrain. They are betting that identifying the right patient (no Alzheimer’s plaques) makes the mechanism relevant.

Manufacturing/CMC Risks: This is the core of the investment thesis.

The Claim: “Batch A” capsules (used in the failed placebo-controlled phase) contained a mixture of polymorphic forms. Over time (aging), the active ingredient converted to a less soluble form, leading to underdosing.

The Fix: “Batch B” (used in the successful extension) used a stable polymorph with proper bioavailability.

Assessment: Scientifically, this holds water. Polymorphs can drastically alter solubility (look up Ritonavir for a famous example). However, it implies their original CMC work might have been sloppy. They must demonstrate to the FDA that they can manufacture the stable form consistently for Phase 3.

Clinical Data

Efficacy (The Failed Primary):

Headline: The placebo-controlled Phase 2b (16 weeks) failed to show a statistically significant difference on the primary endpoint (CDR-SB).

The Save: In the 32-week extension (open-label), patients switched to “Batch B” (the good pills) showed a 65% reduction in clinical worsening compared to those on “Batch A” (the bad pills).

Biomarker Support: Plasma GFAP (a marker of neurodegeneration) dropped significantly (-16.0 pg/mL) in the Batch B group, correlated with clinical benefit. This suggests biological activity, not just noise.

P-Hacking Check:

Red Flag: The positive data comes from comparing two arms in an open-label extension, not the randomized phase.

Subgroup Mining: The best results are in patients with plasma ptau181 < 21.0 pg/mL (pure DLB). While biologically rational (removing AD patients removes noise), this is a post-hoc slice. Phase 3 will use this as an inclusion criterion, which reduces the Total Addressable Market (TAM) but increases Probability of Success (PoS).

Safety/Tolerability:

Liver Toxicity: Liver enzyme elevations occurred in 2.5% of patients in the initial phase and 1.3% in the extension. While reversible, p38 inhibitors are liver-toxic. In a larger Phase 3, if a patient goes into liver failure, the trial likely halts. This is a material risk.

Biochemical Deep Dive

Investors often treat mechanism of action (MoA) as a black box. For CervoMed, you cannot afford to do that. The entire bull case rests on a specific, somewhat complex biological hypothesis: that Dementia with Lewy Bodies (DLB) is fundamentally different from Alzheimer’s because the damage is reversible.

Here is the breakdown of the science they are betting your money on.

A. The Target: p38 Alpha Kinase

The Villain: p38 alpha (p38α) is an intracellular enzyme that responds to stress and inflammation. In a healthy brain, it’s a temporary signal. In a neurodegenerative brain, it gets chronically stuck in the “on” position.

The Damage Loop: Chronic p38α activation hyper-activates a protein called Rab5.

The Consequence: Rab5 is a traffic cop for the cell’s internal transport system (endosomes). When Rab5 goes rogue, it jams the transport of Nerve Growth Factor (NGF) signals from the synapse back to the cell body. Without NGF signals, the neuron withers — it stops functioning and shrinks (atrophy), but crucially, it does not immediately die.

B. The Cholinergic Rescue Thesis

This is the differentiator. In Alzheimer’s, neurons die due to amyloid plaques and tau tangles (irreversible). CervoMed argues that in pure DLB (patients without Alzheimer’s plaques), the primary pathology is this reversible atrophy of the Basal Forebrain Cholinergic (BFC) system.

The Drug’s Job: Neflamapimod blocks p38α.

The Chain Reaction: Blocking p38α calms down Rab5 → Axonal transport restarts → NGF signals get through → The cholinergic neuron wakes up and regains function.

Why It Matters: This system controls attention, motor function, and memory. If the neurons are just sleeping (atrophied) rather than dead, the drug can show clinical benefit in 3-6 months. If they are dead (as in advanced Alzheimer’s), the drug is useless. This is why the pure DLB exclusion criteria (screening out AD patients) is existential to the trial’s success.

C. The Receipts: Do We Have Proof?

The company points to two key pieces of biological evidence to prove this isn’t just a nice story:

GFAP Reduction: In the Phase 2b extension, plasma GFAP (a biomarker of neuroinflammation and astrocyte reactivity) dropped by 16.0 pg/mL in patients on the “good” drug batch, compared to an increase in the placebo/failed batch group. This correlates with the clinical benefit, suggesting the drug is physically hitting the neuroinflammatory target.

Basal Forebrain MRI: In a separate small study (n=15), they showed MRI evidence of increased volume in the Nucleus Basalis of Meynert (NbM) after treatment. This supports the regrowth/rescue hypothesis, though the sample size is statistically fragile.

D. The Biological Risks (The Bear View)

Toxicity: p38 is expressed everywhere in the body, not just the brain. Inhibiting it can mess with liver function (as seen in the 1.3%-2.5% enzyme elevations) and immune response. Is it possible to inhibit p38 enough to save neurons without damaging the liver in a larger population?

The Rab5 Link: While the p38-Rab5 connection is published in journals like Nature Communications (co-authored by the CEO), it is heavily reliant on the company’s own research ecosystem. Independent validation of this specific cascade in human DLB patients is less abundant than the amyloid/tau theories.

Take: The biology is elegant because it offers a mechanism for reversal of symptoms, not just slowing decline. This justifies the potential for a visible clinical effect in a short (32-week) Phase 3 trial. However, reliance on the pure DLB subset creates a smaller commercial market and a harder-to-recruit trial (high screen failure rate).

Pipeline

Investors love a deep pipeline because it provides diversification. If Drug A fails, Drug B might save the day. CervoMed, however, is a classic pipeline in a pill story. They have one drug (Neflamapimod) doing all the heavy lifting across three indications. If the molecule has a fundamental flaw (safety/toxicity), the entire company goes to zero.

A. Neflamapimod: The Franchise (and the Liability)

Since this is a repurposed p38 inhibitor (formerly Vertex’s VX-745), the company is trying to squeeze as much utility out of it as possible before the patent clock runs out.

Recovery After Ischemic Stroke (The “RESTORE” Trial)

The Thesis: Stroke causes massive inflammation and synaptic damage. Since Neflamapimod supposedly repairs synapses in the basal forebrain, the theory is it could help stroke survivors regain motor function.

The Status: Phase 2, randomized, placebo-controlled trial. Target enrollment: ~90 patients.

The Timeline: Top-line data expected 2H 2026.

Take: Stroke recovery is a notorious graveyard for biotech. While the mechanism makes sense on paper (anti-inflammatory), demonstrating functional recovery in a heterogeneous stroke population is incredibly difficult. Treat this as a free lottery ticket, not a core valuation driver.

Frontotemporal Dementia (FTD)

The Thesis: FTD (specifically the PPA subtype) shares synaptic dysfunction features with DLB.

The Status: Phase 2a open-label study. Small sample size (~20 patients).

The Carrot: FDA granted Orphan Drug Designation for this indication in Nov 2024, which offers tax credits and 7 years of exclusivity if approved.

The Timeline: Biomarker data expected mid-2026.

Take: With n=20, this is a signal-finding study, not a registration trial. It’s useful for generating headlines (e.g., “positive biomarker data!”), but it’s years away from commercial reality.

B. EIP200: The Lifeboat (Preclinical)

The Asset: A “novel co-crystal” of neflamapimod.

The Strategy: This is a classic Medicinal Chemistry 101 tactic. Since the original Neflamapimod molecule is old (Vertex era), CervoMed needs a way to extend patent life if the polymorph patents get challenged. Identifying a preferred “co-crystal” creates new composition-of-matter IP.

The Status: Preclinical.

Analyst Take: This is an insurance policy. If Neflamapimod becomes a blockbuster, generics will attack the patents. EIP200 would likely be the backup plan to evergreen the franchise.

Pipeline Verdict:

Diversification Score: Low. This is not necessarily a diversified biotech. It is a levered bet on the p38 alpha kinase mechanism.

The Risk: Since all three clinical programs use the exact same molecule, a safety signal in one (e.g., liver toxicity in the DLB trial) will likely halt the stroke and FTD trials immediately.

The Batch Contagion: The “bad batch” issue identified in the DLB trial implies that all historical data with this drug should be scrutinized for what formulation was used. Ensure the stroke and FTD trials are using the “Batch B” (stable) formulation, or those trials will likely fail too.

Intellectual Property & The Moat

The Competitive Landscape:

Standard of Care: Acetylcholinesterase inhibitors (generic, cheap).

Competition: The DLB pipeline is sparse compared to Alzheimer’s. Most competitors are repurposing AD drugs (anti-amyloids), which CervoMed argues don’t work in pure DLB. This should give them a blue ocean strategy if they succeed.

The summary below is based on the Form 10-K filed March 2025.

Summary

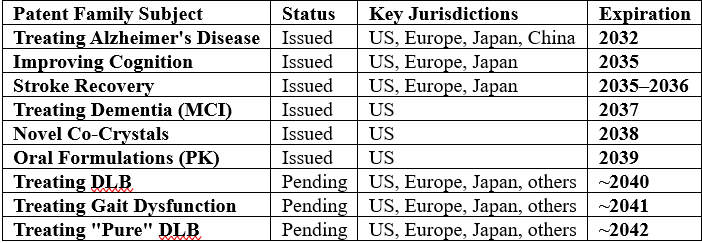

CervoMed does not appear hold a valid composition-of-matter patent for the neflamapimod molecule itself; the original patent covering the chemical structure (licensed from Vertex) appears to have expired in 2017. Instead, the company relies on a portfolio of 10 wholly owned patent families covering specific uses, formulations, and crystal forms of the drug, with expiration dates extending into the 2030s and 2040s.

Key Patent Families & Expiration Dates

CervoMed wholly owns the following key patent families:

Strategic Context & Potential Risks

Lack of Composition of Matter: Because the core molecule patent expired in 2017, CervoMed appears to relies on “use” patents (e.g., using the drug specifically for DLB) and formulation patents. The company acknowledges that these are generally narrower in scope and harder to enforce than composition-of-matter patents, potentially increasing the risk of generic competition or litigation.

Vertex License: CervoMed appears to hold an exclusive worldwide license from Vertex Pharmaceuticals. While they appear to owe Vertex up to $122 million in potential milestones and “low- to mid-teens” royalties on net sales, these royalties appear to be reduced by 50% during any period where there is no valid patent claim covering the product.

The Verdict

Scientific Conviction: Medium-Low.

The “Batch” explanation is chemically plausible but convenient. The mechanism (p38) is risky.

Commercial Viability: Medium.

Pure DLB is a distinct market, but the diagnostic requirement (blood test for ptau181) adds friction to prescribing.

The M&A Appeal: Medium-Low.

Big Pharma tends to avoid p38 inhibitors (toxicity baggage) and heavy royalty stacks (Vertex gets a big cut). They would likely wait for Phase 3 data before touching this.

Trader Profile: Binary Event Gamblers. This is a play on the Phase 3 funding announcement and subsequent initiation.

Final Verdict: WATCH LIST (Wait for Dilution)

The company is running on fumes. They must raise capital soon. The stock price will likely suffer during the raise. The time to enter seems to be after the financing removes the immediate bankruptcy risk, assuming the valuation resets to a level that accounts for the 2+ year wait for Phase 3 data.

The BUY Case (The Believer)

The Thesis: You believe the “batch theory“ is scientifically sound — polymorph aging killed bioavailability in Phase 2b, and the “good pills” (Batch B) genuinely unlock the drug’s efficacy. You accept the hypothesis that pure DLB (no Alzheimer’s co-pathology) is a distinct biological bucket where p38 inhibition works.

The Upside: If Phase 3 replicates the open-label extension data (65% reduction in clinical worsening), CervoMed becomes the first company to crack the DLB code. With no approved treatments and a desperate patient population, the stock could 10x from current distressed levels.

Target Investor: The Binary Event Gambler. You are comfortable holding through massive volatility and dilution because you are playing for a potential buyout or commercial monopoly in 2027+.

The SELL Case (The Skeptic)

The Thesis: You know that post-hoc subgroup analyses of open-label extension studies have a 90%+ failure rate in Phase 3. You suspect the “Batch B” success was a placebo effect or selection bias (healthier patients survived to the extension). You are terrified of the liver toxicity signal (1.3% - 2.5% enzyme elevations) appearing in a larger trial and causing a clinical hold.

The Downside: The company has less than 12 months of cash and plans to start an expensive 300-patient trial in late 2026. If the financing fails or comes with toxic terms (warrant coverage, high liquidation preference), current equity gets wiped out. If the trial fails, the IP would be worthless.

Target Investor: The Fundamentalist. You see a repurposed molecule with a heavy royalty burden and creative data interpretation. You stay away.

The HOLD / WATCH LIST Case (The Sniper)

The Thesis: The science is plausible enough to be interesting, but the timing is wrong. The dilution gap is undeniable: they have ~$27M and burn ~$8M/quarter, meaning they must raise capital before starting Phase 3 in 2H 2026.

The Strategy: Do not buy yet. Let the inevitable financing happen. Let the dilution hit the share price. Once the company has secured the cash runway to actually finish the Phase 3 trial (likely $50M-$100M needed), the bankruptcy risk is removed.

Target Investor: The Distressed Value Hunter. You are waiting for the de-risked entry point — post-dilution, pre-data.

Final Note:

This is not a simple stock; it is a complex derivative of chemistry, regulatory maneuvering, and cash burn.

Disclaimer: This is not financial advice. I am a chemist and an analyst, not your wealth manager. Biopharma stocks are volatile and can go to zero. Do your own due diligence.

This report is for informational and educational purposes only. It does not constitute investment advice, a recommendation to buy or sell any securities, or an offer to sell or a solicitation of an offer to buy any securities.

The scientific analysis presented here is for investment due diligence purposes only and should not be interpreted as medical guidance, diagnosis, or treatment recommendations.

At the time of writing, the author does not hold a position in CervoMed (CRVO).

Biotech investing is highly volatile and involves the risk of total loss. Past scientific validation does not guarantee future clinical success. Regulatory hurdles, clinical failures, and market conditions can materially affect the value of these securities.

For informational and educational purposes only — not investment advice. The author's position (if any) is as stated in the original article. Always verify against primary sources and do your own due diligence.