Aptevo Therapeutics (APVO) - Scientific Deep Dive for Mipletamig, ALG.APV-527, and the ADAPTIR Pipeline

Executive Summary

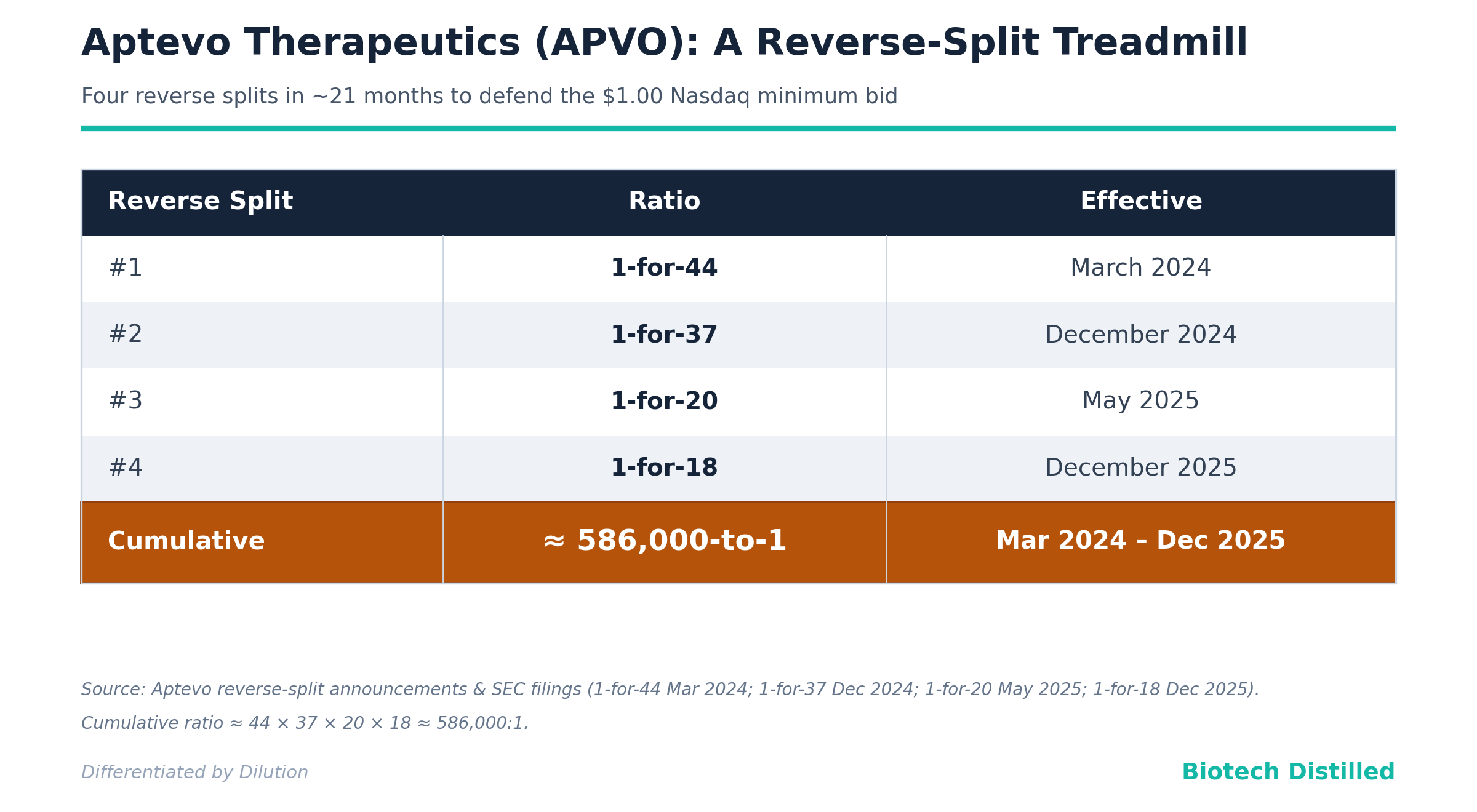

The Hook. Aptevo is selling a CD123 x CD3 T-cell engager (mipletamig) whose headline “79–81% remission” comes from 28–31 evaluable frontline AML patients with no randomized control arm, wrapped inside a corporate shell that has executed four reverse stock splits in roughly 21 months to stay listed.

The Bull Case. Mipletamig has, to date, shown zero cytokine release syndrome (CRS) in frontline AML patients treated in combination with venetoclax + azacitidine (“ven/aza”) — a genuinely notable result in a drug class (CD123xCD3) that has been repeatedly killed by CRS. If the no-CRS profile holds, mipletamig could in theory be added to the ven/aza standard of care to deepen remissions (including in TP53-mutant patients, who fail ven/aza fast), in a frontline unfit-AML market AbbVie built into a multi-hundred-million-dollar franchise. Orphan designation gives 7-year U.S. exclusivity on approval; the core patent family reportedly runs to ~2037. At a ~$5–11M market cap against $14.5M of cash, the equity is, at moments, valued below net cash — a deep-value optionality argument for the brave.

The Bear Case. This is a financing structure with a science project attached. Cumulative reverse-split ratio since March 2024 is roughly 586,000-to-1 (1-for-44 × 1-for-37 × 1-for-20 × 1-for-18). The stock is down ~98% over twelve months on a split-adjusted basis. The company carries an explicit going-concern qualification, $14.5M cash against ~$8.0M/quarter operating burn, and survives on two Yorkville equity lines ($85M nominal capacity) plus a Roth ATM. The efficacy pitch relies on the evaluable-vs-ITT denominator trick and a cross-trial comparison to VIALE-A that cannot, by construction, prove additive benefit. The lead asset is the former APVO436 — a ~7-year-old molecule in a class (flotetuzumab, vibecotamab, JNJ-63709178) that bigger, better-capitalized players have largely abandoned. The second program (ALG.APV-527) produced zero objective responses (best response: stable disease) and is partner-encumbered and stalled. Six preclinical “shots on goal” plus a freshly announced radiopharmaceutical collaboration read as theme-chasing to support raises, not a funded plan.

Bottom Line. The no-CRS frontline signal is the one real asset here, and it is not enough. Between the dilution mechanics, the unprovable efficacy claim, the class-disadvantaged lead, and going-concern doubt, this is a PASS/AVOID.

Catalyst Calendar & Financial Runway

Upcoming Catalysts (next 12–18 months)

RAINIER Phase 1b completion / Phase 2 dose selection — 2H 2026. RAINIER is a Phase 1b/2 dose-optimization, multi-center, open-label study of up to 51 frontline unfit-AML patients across five dose levels (9 mcg – 137 mcg) of mipletamig + ven/aza; Phase 1b is expected to conclude in 2H 2026, followed by a Phase 2 informed by the recommended Phase 2 dose (RP2D). This is the only near-term value-bearing readout.

ALG.APV-527 dose-expansion decision — undefined. Aptevo and Alligator are “evaluating next steps” after the completed Phase 1 dose-escalation. There is no committed timeline or funding — treat as indefinite.

Q2 2026 financials — ~August 2026. Watch SEPA takedowns and any partnering/milestone receipts.

Niowave radiopharmaceutical collaboration — announced May 27, 2026. New strategic collab; terms not yet detailed. A theme attachment, not a clinical catalyst.

The Dilution Gap — there is no “gap,” there is a chasm.

As of March 31, 2026 the company held $14.5M cash, down from $21.6M at year-end 2025, after using $8.0M in operating activities in Q1 2026.

At that burn, unaided runway is on the order of five to six months — yet management guides to “into 4Q26,” which is achievable only by drawing the equity lines.

The funding stack:

a First SEPA with Yorkville (June 16, 2025, up to $25M) and a Second SEPA (January 8, 2026, up to $60M), for $85M nominal capacity, ~$67.2M remaining, plus an ATM with Roth Capital (April 28, 2025).

Critically, the ATM is choked by the baby-shelf rule (General Instruction I.B.6): with public float under $75M, Aptevo may sell no more than one-third of non-affiliate float per 12 months, with additional capacity not expected until after October 2026. And the company is barely able to use the SEPAs — it drew only $0.9M net in Q1 2026 (plus $0.2M subsequent), because at a single-digit share price every draw is brutally dilutive.

A raise is not “likely before the next data drop” — the company is in a continuous, structural raise, punctuated by reverse splits to defend the $1.00 Nasdaq minimum bid.

The reverse-split cadence is the receipt that matters:

Insiders & Institutions — the wrong signals. In short, no specialist biotech fund (Fairmount, RA Capital, Baker Bros, Perceptive, Deep Track, Avoro, EcoR1, Vivo, Adage) holds a 13D/13G here. The historical “institutional” names are Armistice Capital and Sabby Management — microcap PIPE/warrant financiers, not conviction capital — and a Bank of America 13G (15.0%, shared voting/dispositive power, “ordinary course”) that is custodial, not directional.

The Science: Mechanism & Chemistry

Two clinical-stage biologics.

Mipletamig (formerly APVO436) is a CD123 x CD3 bispecific built on the ADAPTIR platform — a single-gene, antibody-backbone homodimer with an IgG1 Fc (silenced to eliminate FcγR binding) and scFv binding domains.

ALG.APV-527 is a 4-1BB x 5T4 bispecific on the same ADAPTIR scaffold. The six preclinical assets use ADAPTIR or the newer ADAPTIR-FLEX heterodimer (two-gene, knob-in-hole) format that can bind up to four targets.

These are bispecific/trispecific T-cell and co-stimulatory engagers — a crowded, well-trodden field.

Mechanism validation. CD123 is a validated target: it is over-expressed on AML blasts and, importantly, on leukemic stem cells, and tagraxofusp (Elzonris, Stemline/Menarini) — a CD123-directed cytotoxin — is FDA-approved in BPDCN. But validation of the target is not validation of the approach. Redirecting T cells against CD123 in AML is a graveyard: the question mipletamig must answer is not “is CD123 a real target” (yes) but “can a CD123xCD3 engager add benefit without unacceptable CRS” — where the entire class has stumbled.

Manufacturing / CMC. ADAPTIR molecules use antibody-like CHO manufacturing. Management touts “extremely low cost per dose” from microgram dosing — plausible for a T-cell engager, and not the risk here. CMC is not the quiet killer; the balance sheet is.

Biochemical Deep Dive

The Target. CD123 (IL-3 receptor α-chain) is over-expressed on AML blasts and leukemic stem cells (LSCs), making it attractive because LSCs drive relapse. The therapeutic logic: crosslink a patient’s T cell (via CD3) to a CD123⁺ leukemic cell, triggering redirected T-cell cytotoxicity (RTCC). The catch baked into the biology: CD123 is also on normal hematopoietic and dendritic/basophil populations, and T-cell engagement against a high-burden, cytokine-primed leukemic compartment is exactly what drives CRS.

The Chemistry. Mipletamig is a (scFv)₄-Fc construct: two CD123 scFv and two CD3 scFv arms on a homodimeric IgG1 Fc, with Fc silencing mutations to prevent FcγR-mediated T-cell crosslinking, and FcRn recycling preserved for an antibody-like half-life (~84 h in preclinical models). The differentiating design choice is the CRIS-7-derived, bivalent CD3 domain, which the company reports induces lower cytokine secretion than competitor CD3 binders while retaining potency at microgram doses. This is the entire scientific thesis: same target as a failed class, but a CD3 arm tuned to blunt CRS.

The Mechanism. Activated T cells, crosslinked via CD3 to CD123⁺ blasts, lyse the target. In the frontline RAINIER design, mipletamig is layered on top of ven/aza — the BCL-2-inhibitor + hypomethylating-agent backbone that already drives deep remissions — so the incremental mechanism (extra T-cell-mediated blast clearance / deeper MRD negativity) is what must justify the drug. With no control arm, that increment is asserted, not measured.

The Biomarker Receipts. For mipletamig the translational evidence is thin in the public materials: the headline is the absence of a pharmacodynamic problem (no frontline CRS) rather than positive target-engagement biomarkers. For ALG.APV-527 there is cleaner mechanistic confirmation — dose-proportional exposure in all patients, soluble 4-1BB changes, and biopsy data showing 5T4 expression with increased intratumoral T cells. Useful biology; unfortunately attached to a drug with no objective responses.

Bottom line for the thesis: the science is coherent — a CD3-tuned engager to escape the class’s CRS trap is a legitimate idea, and the no-CRS frontline data is the proof-of-concept for that idea. But “we didn’t cause CRS” is a safety receipt, not an efficacy receipt, and the investment case requires the latter against a control arm that does not exist.

Clinical Data

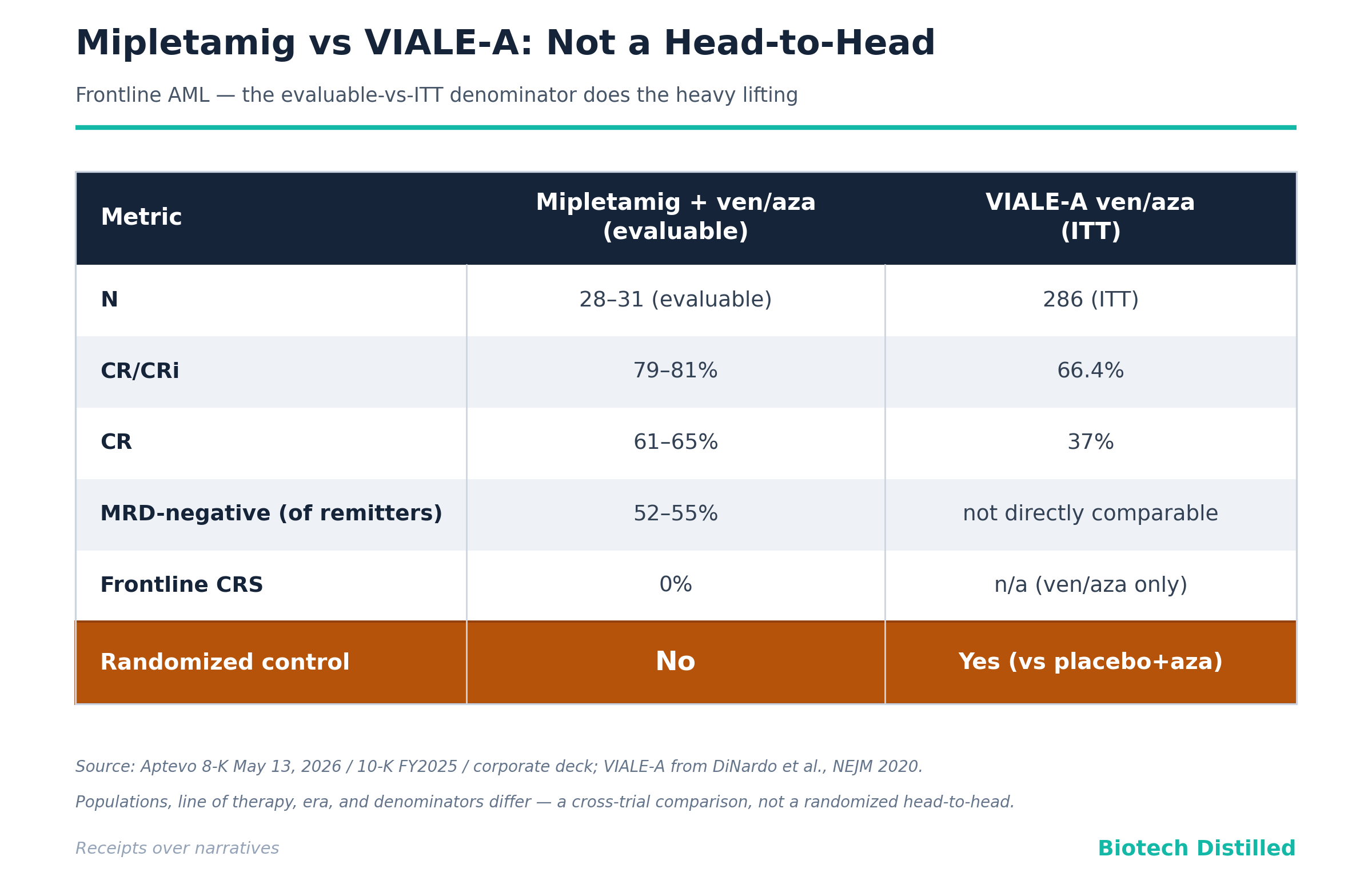

Efficacy — the denominator does the heavy lifting. The frontline pitch (most recent cut): among 31 evaluable frontline patients (mipletamig + ven/aza), 87% clinical benefit, 81% CR/CRi, 65% CR, 52% MRD-negative, no CRS. Management benchmarks this against VIALE-A (the registrational ven/aza trial): 66.4% CR/CRi and 37% CR in the 286-patient ITT ven/aza arm, with median OS 14.7 months vs 9.6 months on placebo+aza (HR 0.66).

Cross-trial comparison caveat — and it is doing all the work here. This is not a head-to-head.

Evaluable vs ITT: mipletamig’s 79–81% is computed on patients who survived and were assessable; VIALE-A’s 66% is intent-to-treat, which includes early deaths and dropouts. Evaluable-only denominators systematically inflate response rates.

No control arm: RAINIER is single-arm — there is no randomized ven/aza comparator within the trial, so the “additive benefit” claim is structurally unprovable.

N is tiny: the 95% confidence interval around 79% in 28 patients runs roughly 60%–92%, which overlaps VIALE-A’s 66.4% — i.e., the point estimate looks better, but the data cannot distinguish mipletamig+ven/aza from ven/aza alone.

The TP53 wrinkle. Aptevo notes 35% of its remitters carried TP53 mutations (poor-prognosis). The implied story is that mipletamig rescues a population ven/aza fails. But the literature is blunt: TP53-mutant AML derives little durable benefit from ven/aza — CR/CRi ~47% but median remission duration ~5.6 months and median OS ~5.2–7.2 months, similar to HMA alone. With 28–31 patients and no durability or OS data, “TP53 patients responded” tells us nothing about the only thing that matters in TP53 AML — how long.

The P-Hacking / framing check. No formal endpoint-shift or post-hoc subgroup p-value to flag (these are descriptive Phase 1b response rates), but the framing games are present: an evaluable denominator benchmarked against an ITT denominator; “clinical benefit” defined to include stable disease; and a “no CRS” headline that omits context.

Safety — the quiet killers, and the one bright spot.

The genuine signal: no CRS in frontline patients to date. That is meaningful for a CD123xCD3. But two caveats.

First, the deck’s “Mipletamig continues to demonstrate a highly favorable safety profile” eludes that CRS did occur in earlier phases — the 10-K states plainly that “CRS cases occurred in some mipletamig patients in both the dose escalation and the dose expansion phases,” with ~26% CRS and ~30% infusion-related reactions in relapsed/refractory patients, consistent with the ~1-in-5 CRS reported for APVO436 at ASH 2021.

Second, frontline ven/aza patients are an inherently cleaner CRS population — lower disease burden after ven/aza cytoreduction, no prior T-cell-engager sensitization — so part of “no frontline CRS” may be the setting, not solely the molecule.

The honest read: encouraging, not yet de-risked.

Monotherapy — weak. Single-agent dose-escalation: 49% “clinical benefit” (19/39) — but that figure includes stable disease; only two complete remissions were observed in 39 patients (~5% CR), with 36% (12/33) showing blast reductions. The waterfall is heavily progressive disease at the top. Monotherapy is a mechanism footnote, not a path.

ALG.APV-527 — no objective responses. Phase 1 dose-escalation, 19 patients across five cohorts: 10/17 evaluable (59%) achieved stable disease as best response; zero PRs or CRs. Favorable safety (no severe liver toxicity), clean PK (terminal t½ ~9 days), and target-engagement biomarkers — but “stable disease” in a single-arm escalation is the weakest possible efficacy currency. The company and Alligator are “evaluating next steps,” which in plain English means neither is committing capital.

Data integrity. Everything here is open-label, single-arm, small-N Phase 1/1b. No blinding, no randomized control, modest patient numbers. Appropriate for early development; inappropriate as the basis for the “superior to standard of care” language the deck flirts with.

Pipeline

Mipletamig (CD123 x CD3) — Phase 1b/2, frontline AML. Orphan-designated (Nov 26, 2019). The only asset carrying the story. Value driver if RAINIER’s no-CRS profile and remission depth survive into a controlled Phase 2; otherwise optionality.

ALG.APV-527 (4-1BB x 5T4) — Phase 1 complete, solid tumors. 50/50 with Alligator Bioscience. Best response = SD; expansion uncommitted. Optionality at best; zero-NPV placeholder more likely given no objective responses and a partner standoff.

Preclinical (six assets), all IND-enabling or earlier, no human data:

APVO603 (4-1BB x OX40) — dual co-stim, tumor-agnostic; IND-enabling.

APVO711 (PD-L1 x CD40) — checkpoint + APC activation.

APVO442 (PSMA x CD3) — prostate, ADAPTIR-FLEX.

APVO455 (Nectin-4 x CD3) — bladder/breast/NSCLC/H&N; newly highlighted.

APVO451 (Nectin-4 x CD40 x CD3) — trispecific; SITC in-vitro data.

APVO452 (PSMA x CD40 x CD3) — trispecific, prostate.

All are “designed to” with preclinical-only support. The 2026 “expansion to trispecifics” and the May 2026 Niowave radiopharmaceutical collaboration widen the narrative surface for financings; they do not constitute a funded, prioritized plan. No RPDD/PRV optionality to score into a SOTP. A company with $14.5M and 33 employees cannot meaningfully advance eight molecules — most of this pipeline is, realistically, zero-NPV until partnered.

Pipeline Verdict. Mipletamig is the valuation, full stop. ALG.APV-527 is encumbered optionality; the six preclinical assets are platform marketing. Strip out mipletamig and there is no investable thesis.

Intellectual Property & The Moat

The summary below is based on the 10-K filed by the Company in March 2026 and the 10-Q filed in May 2026.

Aptevo reports owning or exclusively licensing the patents/applications behind the ADAPTIR and ADAPTIR-FLEX platforms and pipeline assets, with non-exclusive licenses only for research tools (Lonza CHO cell lines/vectors; OMT OmniAb transgenic rodents). The platform IP traces to Trubion (pre-Emergent), with a linker family co-invented with Wyeth and assigned through the Emergent spinoff. Issued ADAPTIR patents span the U.S., Australia, Canada, Hong Kong, Israel, Japan, Mexico, New Zealand, Russia, Singapore, South Africa, and South Korea.

Asset-specific runways (reportedly):

Mipletamig: core patent family nationalized across ~24 jurisdictions; the company reports core-family exclusivity to ~2037. Backstop: orphan exclusivity = 7 years U.S. on approval; biologics enjoy 12-year BPCIA reference-product exclusivity.

ADAPTIR platform: issued/pending patents reportedly expire 2027–2039.

ADAPTIR-FLEX: PCT filed 2021, nationalized 2023; if granted, expire ~2041.

ALG.APV-527: co-owned with Alligator (PCT/EP2018/069850), plus co-owned U.S. 10,239,949 and U.S. 11,312,786, plus an exclusive license from Alligator to a separate family (PCT/EP2017/059656); deck claims exclusivity to ~2038 (+ up to 5 years PTE).

Ownership & licensing structure. Mipletamig is wholly owned. ALG.APV-527 is the encumbrance: joint 50/50 ownership and co-development with Alligator, with opt-out rights at Phase 1a/1b completion, automatic-termination “stage gates,” and, post-opt-out, tiered royalties (low- to mid-single digits) owed by the continuing party. That is a meaningful drag on any future ALG.APV-527 economics and another reason the asset screens as low-value.

Competitive landscape — the shark tank, and the class is thinning.

Affimed, ImmunoGen (AbbVie), Innate/Sanofi, MacroGenics/Gilead, MD Anderson/Xencor, Menarini, Molecular Partners/U-Bern, Lava, Sanofi.

Flotetuzumab (MacroGenics’ CD123xCD3 DART) was effectively shelved in favor of next-gen MGD024

Vibecotamab (Xencor’s XmAb14045) was redirected from active AML to MDS/MRD settings after modest activity and CRS

JNJ-63709178 has been discontinued amid severe CRS and insufficient benefit

Talacotuzumab died for toxicity. Tagraxofusp validates the target in BPDCN but is not a T-cell engager and not approved in AML.

Why this matters for the moat: mipletamig’s differentiation (a CRS-sparing CD3 arm) is aimed squarely at the class’s failure mode, which is the right idea — but it also means Aptevo is the small, undercapitalized survivor in a niche the deep-pocketed players have been exiting, which dampens both the competitive urgency and the M&A logic.

For ALG.APV-527, the 4-1BB/5T4 space is sparse (Crescendo preclinical; Biotecnol/Chiome 5T4xCD3) while broader 4-1BB bispecifics (PD-L1x4-1BB at BioNTech/Genmab and Pieris/Servier in Phase 3; 4-1BBxFAP at Roche/BI/Amgen-Molecular Partners) are further along.

Aptevo’s asset is neither first nor differentiated on data.

The Verdict

Scientific Conviction: Low-to-Medium. The CRS-sparing CD3 thesis is legitimate and the no-frontline-CRS data supports it; but efficacy benefit over ven/aza is unproven, the lead is a class straggler, and the second asset has no objective responses.

Commercial Viability: Low. Even a clean Phase 2 leaves a tiny company years and many dilutive dollars from a BLA in a competitive frontline-AML market AbbVie owns (ven/aza, plus pivekimab).

M&A Appeal: Low. Nothing here a strategic needs. The logical AML buyer (AbbVie) already owns the backbone and a CD123 ADC; CD123xCD3 is a class others are leaving; ALG.APV-527 is partner-encumbered; the platform has produced no approved drug in the ~10 years since the Emergent spinoff. Retail “buyout after the reverse split” hope is not a thesis.

Trader Profile: Binary-event and reverse-split-bounce gamblers only. The microcap float and ~$5–11M market cap mean there is no meaningful options chain to express views with defined risk; this is a momentum/news-trading instrument, structurally hostile to buy-and-hold.

Buy (speculative only).

Target audience: deep-value microcap specialists comfortable with total-loss risk.

Rationale: the equity occasionally trades below net cash (EV near zero/negative), there is a genuine no-CRS frontline signal, and a clean RAINIER readout in 2H 2026 could spark a violent short-term repricing off a microcap base.

Execution/Strategy: this is a trade, not a position — size as a lottery ticket you can lose entirely, define a hard stop, and plan to sell the news into any RAINIER pop rather than hold through the inevitable follow-on financing. Do not anchor to the share price through reverse-split events.

Hold.

Target audience: essentially nobody on fundamentals.

Rationale: a “hold” here is a slow bleed — the structural dilution and reverse-split treadmill mean time is the enemy of the long.

Execution/Strategy: if you own it and are not actively trading the catalyst, the default action is to use strength to exit; “hold and wait” in a serial-diluter is how positions go to ~zero.

Sell / Avoid.

Target audience: every fundamentally-driven investor.

Rationale: going-concern doubt, ~$8M/quarter burn on $14.5M cash, four reverse splits in ~21 months (~586,000:1 cumulative), an unprovable efficacy claim on a class-disadvantaged lead, a stalled second asset, and an unfunded preclinical wishlist.

Execution/Strategy: avoid the common entirely.

Final Verdict

PASS/AVOID. A serial-dilution microcap with a CRS-sparing-but-unproven CD123xCD3 in a class larger players are abandoning, an evaluable-vs-ITT efficacy pitch that cannot demonstrate additive benefit without a control arm, a stalled partner-encumbered second program, and an explicit going-concern qualification — the one real asset (no frontline CRS) cannot carry the structure.

This report is strictly for informational and educational purposes only. It does not constitute financial advice, investment advice, or a recommendation to buy or sell any securities mentioned.

The scientific and clinical analyses herein should not be interpreted as medical guidance, diagnostic information, or treatment recommendations.

At the time of writing, the author does not hold a position in Aptevo Therapeutics (APVO).

Biotech investing is inherently volatile. Past scientific validation does not guarantee future clinical or regulatory success. Treat all clinical-stage biopharma allocations accordingly.

For informational and educational purposes only — not investment advice. The author's position (if any) is as stated in the original article. Always verify against primary sources and do your own due diligence.