Compugen Ltd (CGEN) — Scientific Deep Dive for COM701, GS-0321 and the Unigen Pipeline

Executive Summary

The Hook. Compugen is a computationally-discovered checkpoint shop whose two best assets — a PD-1/TIGIT bispecific in 10+ Phase 3 trials and an anti–IL-18-binding-protein antibody in Phase 1 — are owned by AstraZeneca and Gilead, while the asset it still owns (COM701, anti-PVRIG) is being bet on a monotherapy-maintenance thesis built almost entirely on a post-hoc subgroup.

The Bull Case. At ~$2..00–2.80/share and ~94.6M shares, the market cap is roughly $200–265M against $134.9M of net cash and no debt. That is an enterprise value of roughly $85–130M for: (i) a derived royalty plus up to $195M in milestones on rilvegostomig, an AstraZeneca PD-1/TIGIT bispecific AZ pegs at a non-risk-adjusted >$5B peak-year-revenue target that just posted a 70% confirmed ORR in 1L HER2+ gastric; (ii) up to $758M of remaining milestones plus single-to-low-double-digit royalties on GS-0321, the IL-18BP antibody Gilead paid to license; and (iii) an owned, randomized COM701 trial with a Q1 2027 readout. If COM701 hits and rilvegostomig converts even partially, the sum-of-the-parts (SOTP) dwarfs today’s EV.

The Bear Case. COM701’s pivot to single-agent maintenance in platinum-sensitive ovarian cancer (PSOC) rests on a couple of durable partial responses in immune-desert patients and a post-hoc “no-liver-mets” subgroup from a 60-patient Phase 1 pool — thin monotherapy evidence to carry a placebo-controlled median-progression-free-survival (mPFS) endpoint. COM902, the anti-TIGIT, has effectively been shelved by management’s own admission after the TIGIT field collapsed. Rilvegostomig is a PD-1/TIGIT bispecific in a class that is a graveyard (Roche, Merck, Arcus/Gilead all failed). The “AI/ML platform” valuation is, today, essentially zero. If MAIA-ovarian misses, you are left holding cash plus partnered optionality of uncertain timing.

Bottom Line. This is a rare small-cap that is not facing a dilution gap into its catalyst, and whose downside is meaningfully cushioned by cash (~$1.43/share net). But the owned, value-driving binary (COM701 monotherapy) is leaning on a subgroup, and the partnered upside sits inside a checkpoint class the market has learned to distrust.

Catalyst Calendar & Financial Runway

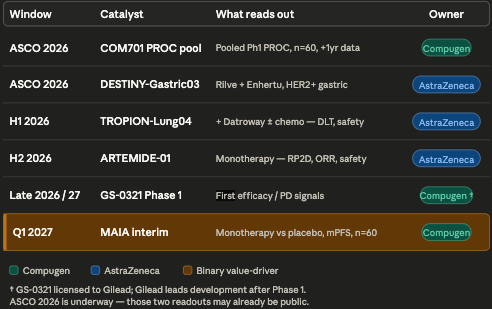

Upcoming Catalysts (next 12–18 months)

The Q1 2027 MAIA-ovarian interim is the binary event. Everything before it is partner-driven de-risking that helps the narrative but does not move Compugen’s owned-asset thesis.

The Dilution Gap — Notably Absent. Compugen ended Q1 2026 with $134.9M in cash, cash equivalents, short-term deposits and marketable securities, and no debt. Management guides runway into 2029 without further inflows. Q1 2026 net loss was $7.7M ($0.08/share), with R&D of $6.9M and G&A of $2.3M; cash fell ~$10.7M from the $145.6M at year-end 2025. At a ~$30–40M annual burn, the company clears the Q1 2027 catalyst — and well beyond — without a raise. There is an F-3 shelf on file for optionality, but the math says they don’t need it near-term. For a clinical-stage biotech walking into a binary, the absence of a forced pre-data raise is a genuine, unusual positive.

The balance sheet was rebuilt by deal-making, not equity. In December 2025, Compugen took a $65M upfront to monetize a portion of its future rilvegostomig royalty and broaden AZ’s TIGIT-bispecific rights. That payment flipped 2025 to a $35.3M net profit on $72.8M revenue (vs. net losses of $14.2M in 2024 and $18.8M in 2023). Read it for what it is: management traded a slice of future royalty upside for present non-dilutive cash. With runway already into 2029, that is balance-sheet armor, not desperation — but it does cap some of the rilvegostomig tail.

Insiders & Institutions. Here the receipts are thin, and that itself is the signal. The notable historical >5% holder is ARK Investment Management (~11% in early 2022 filings) — an innovation/growth manager, not a dedicated immuno-oncology crossover. The float skews generalist/index plus an Israeli institutional and retail base. Translation: the smart-money biotech clustering I normally hunt for is absent. That is a yellow flag for anyone who weights crossover conviction — and, conversely, part of why the stock trades near cash.

Governance note: a CEO transition has occurred — Eran Ophir is now President & CEO, with founder-era leader Anat Cohen-Dayag moving to Executive Chair. Michele Holcomb, Ph.D., joined the board in February 2026. The scientific bench is elite for a company this size: SAB chaired by Drew Pardoll, with Antoni Ribas, Iain McInnes and Anthony Tolcher, plus ex-BMS R&D leaders Nils Lonberg and Elliott Sigal as advisors.

The Science: Mechanism & Chemistry

Everything here is a monoclonal antibody (mAb) discovered against targets that Compugen’s Unigen computational platform nominated. COM701 (anti-PVRIG) is positioned as potential first-in-class; GS-0321 (anti–IL-18-binding-protein) as potential first-in-class; COM902 (anti-TIGIT) as a “best-in-class” Fc-reduced antibody whose chief surviving value is the rilvegostomig franchise.

Mechanism Validation — a split decision. The targets sit on very different rungs of the de-risking ladder:

PD-1/TIGIT (rilvegostomig): PD-1 is one of the most validated targets in oncology; TIGIT is the least validated of the “next” checkpoints after a wall of Phase 3 failures. Rilvegostomig’s bet is that a bispecific with a reduced-Fc design behaves differently than the failed bivalent anti-TIGIT add-ons.

PVRIG (COM701): target validation is preclinical and Phase 1; no approved drug yet de-risks it. The biology (DNAM-1 axis, below) is elegant but unproven in a randomized setting.

IL-18 pathway (GS-0321): the biology of IL-18 is validated (it’s a potent immunostimulatory cytokine), but recombinant IL-18 has failed for 30 years; GS-0321’s wager is that the failure was delivery, not target.

The Cringe Test. Compugen brands hard on “AI/ML-powered Unigen” and “From Code to Cure.” Normally that triggers the buzzword alarm. However, Unigen actually nominated PVRIG, the TIGIT antibody that became an AstraZeneca Phase 3 asset, and the IL-18BP target Gilead paid up to $848M to license. That is more clinical receipts than most “AI drug discovery” stories can show. The cringe is not that the platform is fake — it’s that the current valuation gives the platform zero credit, which is the more interesting fact.

Manufacturing / CMC Risks. Standard antibody risks — Compugen owns no manufacturing and relies on contract manufacturers for COM701, COM902 and GS-0321, with no qualified backup supplier disclosed. Compugen flags this explicitly as a single-source vulnerability.

Biochemical Deep Dive

The Target

COM701 blocks PVRIG (also called CD112R), an inhibitory receptor on T and NK cells that preferentially binds the ligand PVRL2 (CD112/PVR-L2). PVRIG and TIGIT form the two arms of the DNAM-1 axis — parallel, complementary brakes on T-cell activity. The differentiating biology: PVRL2 is reportedly more dominant than PVR (TIGIT’s ligand) on ovarian, breast and endometrial tumors, and PVRIG is preferentially expressed on early-differentiated stem-like memory T cells (Tscm) and dendritic cells (DCs), whereas TIGIT skews to regulatory T cells (Tregs). That places PVRIG upstream, in lymph nodes and tertiary lymphoid structures, rather than only in the inflamed tumor — the rationale for activity in “cold,” immune-desert tumors like ovarian.

The Chemistry

COM701 is a humanized IgG4 with reported high affinity (2 pM KD by KinExA), favorable linear pharmacokinetics, and PVRIG receptor occupancy above a 90% threshold for 21 days at just 1 mg/kg. The IgG4 backbone is a deliberate choice: it avoids the effector-mediated depletion of the very CD8+ T cells the drug is trying to unleash. COM902 takes the same philosophy further — a fully human IgG4 (S228P) anti-TIGIT with femtomolar affinity (626 fM KD) and reduced Fc function, designed to not deplete TIGIT-high lymphocytes. This Fc-attenuation thesis is the same one AstraZeneca leaned on for rilvegostomig (a reduced-Fc IgG1 bispecific), where the company reports unmodified/enhanced Fc actually hurt anti-tumor activity in NSCLC explants.

The Mechanism

The proposed rewiring: PVRIG blockade de-represses Tscm priming by DCs in lymph nodes/TLS → clonal T-cell expansion → infiltration into cold tumors → those tumors become sensitized to anti-PD-1 and anti-TIGIT.

GS-0321 works one cytokine over: IL-18 is a pro-inflammatory, T/NK-activating cytokine, but tumors upregulate IL-18BP, an endogenous decoy that mops up free IL-18. GS-0321 binds IL-18BP and liberates the patient’s own IL-18 preferentially in the tumor microenvironment, rather than dosing recombinant cytokine systemically.

The Biomarker Receipts

This is where COM701 has its most credible data. In a PD-L1-negative, immune-desert ovarian patient with a partial response lasting >18 months, Compugen reports on-treatment increases in peripheral IFNγ and proliferating (Ki67+) CD8 memory and NK-T cells. In a nivolumab-refractory patient, on-treatment biopsies showed CD8+ infiltration rising from 15.7% to 25.7% of tumor area. And TCR-β sequencing showed clonal expansion in clinical-benefit patients regardless of baseline inflammation.

For GS-0321, the proof is preclinical: the surrogate anti-mouse IL-18BP antibody drove monotherapy tumor growth inhibition of 83% (E0771 breast), 58% (MC38ova colon) and 54% (B16F10 melanoma), and — critically — did not cause the splenomegaly or systemic cytokine spikes seen with engineered IL-18.

Bottom Line for the thesis. The pharmacodynamic receipts say the drugs engage their targets and move immune biology in humans (COM701) or in mice (GS-0321). What they do not yet prove is that target engagement translates into a placebo-controlled survival benefit in the setting that matters. Biomarker activation is necessary, not sufficient — and the Q1 2027 readout is where biology meets the denominator.

Clinical Data (COM701)

Efficacy. COM701’s human data is Phase 1, in heavily pretreated platinum-resistant ovarian cancer (PROC) — patients who typically don’t respond to immunotherapy at all:

COM701 + nivolumab + BMS-986207 (anti-TIGIT), n=20: ORR 20% (4 PR, 0 CR), DCR 45%.

COM701 + pembrolizumab + COM902, n=24: ORR 17% (1 CR, 3 PR), DCR 46%.

mPFS in clinical-benefit patients ~10.5 months.

Against the relevant comparators in PROC: anti-PD-1 ± anti-TIGIT runs <10% ORR all-comers and 0% in PD-L1<1; single-agent chemotherapy is ORR ~12–16%, mPFS ~3–4 months, mOS ~13 months. So a ~17–20% ORR with durable benefit in immunotherapy-cold patients is a real signal versus checkpoint monotherapy — but it sits in triplet combinations, not the monotherapy that MAIA will test. For context on what a good PROC drug looks like, AbbVie’s Elahere (mirvetuximab soravtansine) in FRα-high PROC posted MIRASOL Phase 3 ORR of 42% vs 16%, mPFS 5.6 vs 4.0 months, and mOS 16.5 vs 12.7 months (HR 0.67) — the first OS win in PROC (AbbVie/MIRASOL, NEJM/SGO 2025). COM701 is playing a different game (immune mechanism, maintenance, PD-L1-agnostic), but Elahere sets the bar buyers will compare against.

The P-Hacking Check. The entire MAIA-ovarian design is reverse-engineered from a post-hoc subgroup. In the pooled Phase 1 PROC analysis, patients without liver metastases derived clinical benefit 91.3% (21/23) of the time vs 37.8% (14/37) with liver mets. MAIA accordingly excludes liver-metastasis patients. That is a textbook subgroup-to-pivotal leap: it may reflect real biology (liver mets as an immune-suppressive sink) or it may be a small-n artifact that won’t replicate.

Compounding flags: “clinical benefit” is defined as CR+PR+SD>180 days — a soft composite that inflates response framing; the n’s are 20–24 per arm; and the cross-trial chemo benchmarks are historical, not concurrent. The single-agent monotherapy evidence — the actual thing MAIA tests — is essentially two durable PRs in immune-desert patients. MAIA is a bet that a hand-picked population plus a post-hoc subgroup converts a thin monotherapy signal into a placebo-beating mPFS.

Safety / Tolerability — the cleanest part of the story. Across COM701 ± anti-TIGIT ± anti-PD-1 (data cutoff Oct 2024), Grade ≥3 treatment-related AEs ran 9.5%, with no Grade 4/5 events and treatment-related discontinuations of just 4.9%. In the more heavily pretreated triplets, Grade ≥3 TRAEs were ~20% with 4.4% discontinuations. Most common AEs are Grade 1/2 fatigue, diarrhea, nausea — broadly consistent with approved anti-PD-(L)1s. No black-box-type signals, no ILD/cardiomyopathy flags. For a maintenance setting, where tolerability is everything, this is a genuine asset.

Data Integrity. MAIA-ovarian sub-trial 1 is blinded, randomized 2:1 vs placebo (a real upgrade over the open-label Phase 1), n=60, primary endpoint mPFS, conducted in part in Israel and France. The swing factor nobody can pre-size: the placebo-arm mPFS in a population defined as “responders to platinum, not suitable for bev/PARPi.” Management frames this group as having “no current standard of care” and historical mPFS ~5.5 months — but if untreated/placebo maintenance runs better than expected, a 60-patient trial can miss on noise alone.

Pipeline

COM701 (anti-PVRIG, IgG4) — fully owned. THE value driver. PROC Phase 1 done; now in MAIA-ovarian adaptive platform trial, sub-trial 1 (monotherapy maintenance in relapsed PSOC, n=60, 2:1 vs placebo, FPD July 2025, interim Q1 2027). Reality check: this is the only owned, near-term value-creating binary. Carries most of the equity’s owned-pipeline value.

GS-0321 (anti–IL-18BP, formerly COM503) — licensed to Gilead. First-in-human Phase 1 (NCT06759649), dose escalation/expansion as monotherapy and with zimberelimab (Gilead anti-PD-1); FPD January 2025; Compugen runs Phase 1, then Gilead takes over fully. Deal: up to $848M ($90M already received — $60M upfront + $30M IND milestone — plus up to $758M future), single-digit to low-double-digit royalties. Reality check: a de-risked-by-Gilead option with no efficacy data yet. Real optionality, zero near-term proof.

Rilvegostomig (PD-1/TIGIT bispecific) — AstraZeneca, derived from COM902. 10–11 Phase 3 trials plus ~14 Phase 1/2 across NSCLC, GI, biliary, gastric, endometrial. AZ’s non-risk-adjusted peak-year-revenue target is >$5B. Early 1L HER2+ gastric (rilvegostomig + Enhertu + chemo) reportedly hit 70% confirmed ORR (82% in PD-L1 CPS≥1). Compugen is eligible for up to $195M milestones plus tiered royalties to mid-single-digit (partially monetized). Reality check: the highest-expected-value asset, but Compugen is a royalty/milestone passenger, not the driver — and it’s a TIGIT bispecific (class overhang).

COM902 (anti-TIGIT, IgG4) — fully owned, but DEPRIORITIZED. The May 2026 deck still markets COM902 as “potential best-in-class anti-TIGIT”. The March 2026 20-F says the quiet part out loud: after Arcus/Gilead’s STAR-221 futility, the company “currently believe[s] that COM902 has a limited potential to create near-term value to us. We therefore do not plan to initiate new clinical trials with COM902.” Reality check: COM902’s standalone value is roughly zero-NPV; its residual worth is embodied in the rilvegostomig royalty and the retained PVRIG/TIGIT bispecific rights Compugen kept in the AZ amendment.

Early-stage Unigen pipeline — undisclosed. Optionality only.

Pipeline Verdict. The valuation is carried by COM701 (owned, binary) and the partnered tails (rilvegostomig + GS-0321). COM902 is a placeholder. No Rare Pediatric Disease Designation / Priority Review Voucher is in play here, so no PRV add to the SOTP. The honest SOTP: cash floor (~$135M) + a heavily risk-adjusted rilvegostomig royalty + a Gilead-option value + a COM701 lottery ticket — which is precisely why the EV sits near cash.

Intellectual Property & The Moat

The summary below is based on the Form 20-F filed by the Company in March 2026, supplemented by the May 2026 corporate deck.

Compugen reports issued and pending patents covering PVRIG antibodies for cancer treatment, plus COM701 composition-of-matter, use, and combination claims worldwide; and issued/pending COM902 composition-of-matter, use, and combination patents worldwide. COM701 and COM902 were internally discovered and are wholly owned — meaning no inbound royalty stack on the owned programs. The IL-18BP antibody IP (GS-0321) is owned by Compugen and exclusively out-licensed to Gilead; the COM902-derived TIGIT component is licensed to AstraZeneca.

The material recent IP event — EPO opposition. This is the concrete receipt. A European opposition was filed against Compugen’s PVRIG patent. GSK withdrew from the opposition; at oral proceedings on December 3–5, 2025, the EPO opposition division upheld the patent in amended form, with the amended claims now covering functional monoclonal anti-PVRIG antibodies competing with COM701 for cancer treatment. The opponent may appeal, and there is no guarantee of success in this or other proceedings. Net read: the EU PVRIG franchise survived but was narrowed — a partial win, with appeal risk live.

Competitive Landscape. Three distinct battlefields:

TIGIT (rilvegostomig, COM902): a graveyard. The 20-F itself lists the carnage — Roche’s tiragolumab failures (SKYSCRAPER-06/07/03/14), Merck’s vibostolimab failures (Keyvibe-008/010/002), Arcus/Gilead’s domvanalimab STAR-221 futility (Dec 12, 2025), and pembrolizumab’s KEYNOTE-867. Roche and BeiGene have closed their TIGIT programs. Rilvegostomig’s entire pitch is that a reduced-Fc bispecific escapes the class’s fate; the gastric data is the first real evidence it might.

PVRIG (COM701): a lead, but crowding. COM701 is the most advanced anti-PVRIG (Phase 1 + randomized). Clinical-stage competitors are mostly Chinese bispecifics: BioNTech’s BNT3213/PM-1009 (ex-Biotheus, PVRIG/TIGIT bispecific, Phase 1), Simcere’s SIM-0348 (TIGIT/PVRIG bispecific), Hefei TG ImmunoPharma’s NM1F; preclinical entrants include Hengrui (SHR-2002), Shanghai Junshi (JS-209) and FutureGen (FG-B902/T903). The moat is “first and only monospecific PVRIG in a randomized trial” — durable only if MAIA validates the target.

IL-18 (GS-0321): genuinely differentiated. The more-advanced IL-18-pathway competitors are not anti-IL-18BP antibodies — they’re recombinant/cytokine approaches: Simcha’s ST-067 (decoy-resistant IL-18, Phase 1/2), Bright Peak’s BPT-567 (PD-1/IL-18 immunocytokine, Phase 1/2a), and four IL-18-armored CAR-Ts. GS-0321’s anti-IL-18BP antibody mechanism has no named direct clinical competitor — its differentiation is real, which is presumably why Gilead paid up.

COM701’s MAIA setting (PSOC maintenance): the 20-F flags competing Phase 3s in overlapping populations — AbbVie’s GLORIOSA (mirvetuximab + bev), Merck’s TroFuse-022 (sacituzumab tirumotecan ± bev), and Genmab’s RAINFOL-04 (Rina-S + SOC), plus the risk that ADCs and pembro migrate into maintenance after PROC successes. COM701’s specific niche — CR/PR post-chemo patients not suitable for bev/PARPi — is genuine white space, but it is a narrow carve-out that larger franchises could encroach on.

The Verdict

Scientific Conviction: Medium. Elegant, target-engaged biology with human PD receipts (COM701) and a differentiated IL-18BP mechanism (GS-0321) — but the owned binary leans on a post-hoc subgroup and thin monotherapy data.

Commercial Viability: Medium. Real unmet need in PSOC maintenance and a clean tolerability profile; offset by a narrow target population and big-pharma franchises circling the setting.

M&A Appeal: Medium. AstraZeneca is the logical consolidator — it already owns the rilvegostomig franchise and keeps tightening the relationship (the Dec 2025 royalty monetization). Gilead controls the IL-18BP asset. A clean COM701 readout could draw checkpoint-heavy I-O buyers (BMS — a former partner with DNAM-1 history; Merck). Near cash, the optionality alone makes it cheap to look at.

Trader Profile. Two camps: (1) deep-value/sum-of-the-parts investors who like buying a partnered Phase 3 royalty plus a Gilead option for roughly cash, and (2) binary-event traders positioning for the Q1 2027 MAIA readout.

BUY thesis.

Target audience: value-oriented, patient capital comfortable with binary biotech.

Rationale: EV of ~$85–130M for a company with $134.9M net cash, a >$5B-PYR-target partnered Phase 3 asset throwing off milestones + royalties, a Gilead-funded IL-18BP option (up to $758M remaining), and a randomized owned readout — with runway into 2029 and no forced raise. Downside is cushioned by ~$1.43/share of net cash on a ~$2.30 stock.

Execution: consider accumulating in the cash-floor zone, treating COM701 as a free call option. Because there’s currently no dilution gap, time is relatively on your side — consider sizing the position to what you can hold through a possible MAIA miss without forced selling.

HOLD thesis.

Target audience: existing holders who bought the partnered story.

Rationale: the rilvegostomig and GS-0321 tails keep maturing on someone else’s dime; you’re not paying to wait, and the next 12 months bring partner data (gastric, lung) that can re-rate the stock without Compugen spending a dollar.

Execution: consider holding the core, letting partner catalysts and the MAIA interim play out. Think twice before adding aggressively until the placebo-arm-mPFS risk on MAIA is better understood.

SELL / AVOID thesis.

Target audience: investors who require crossover sponsorship and de-risked owned assets.

Rationale: the owned value driver (COM701 monotherapy maintenance) rests on a post-hoc subgroup; COM902 is shelved by management’s own words; rilvegostomig lives in a checkpoint class that has humbled Roche, Merck and Arcus; and there is no smart-money biotech cluster validating the setup. “Cheap” can stay cheap for years in royalty-dependent Israeli small-caps.

Execution: if you own it and are uncomfortable with a placebo-controlled coin flip, the trim-pre-binary discipline may apply — consider lightening into any partner-data strength (ASCO gastric, lung readouts) rather than holding full size into the Q1 2027 binary.

Final Verdict

WATCH LIST. A genuinely cheap, cash-cushioned setup with partnered optionality — but the owned, value-driving catalyst (COM701 monotherapy maintenance) leans on a post-hoc subgroup and thin single-agent data, inside a checkpoint class the market distrusts. Worth tracking closely into the partner readouts; revisit sizing ahead of the Q1 2027 MAIA-ovarian interim. (For the value-minded: the near-cash EV makes this a higher-quality watch than most pre-data biotechs — a candidate to accumulate on weakness rather than chase.)

This report is strictly for informational and educational purposes only. It does not constitute financial advice, investment advice, or a recommendation to buy or sell any securities mentioned.

The scientific and clinical analyses herein should not be interpreted as medical guidance, diagnostic information, or treatment recommendations.

At the time of writing, the author does not hold a position in Compugen Ltd (CGEN).

Biotech investing is inherently volatile. Past scientific validation does not guarantee future clinical or regulatory success. Treat all clinical-stage biopharma allocations accordingly.

For informational and educational purposes only — not investment advice. The author's position (if any) is as stated in the original article. Always verify against primary sources and do your own due diligence.