ADC Therapeutics (ADCT) — Scientific Deep Dive for ZYNLONTA and the CD19 ADC Pipeline

Executive Summary

The Hook. ADC Therapeutics sells ZYNLONTA (loncastuximab tesirine-lpyl), a genuinely differentiated CD19-directed antibody-drug conjugate carrying a pyrrolobenzodiazepine (PBD) DNA-crosslinking warhead — and it just ran the confirmatory Phase 3 (LOTIS-5) that was supposed to unlock the 2L+ diffuse large B-cell lymphoma (DLBCL) market. The trial hit its primary endpoint. The stock fell 57% the next session. The gap between “statistically significant” and “clinically meaningful” is the entire thesis.

The Bull Case. ZYNLONTA is a real, FDA-approved product doing ~$74M/yr, the CD19 target is de-risked six ways to Sunday, and LOTIS-5 technically confirmed clinical benefit (PFS, or progression-free survival, HR — hazard ratio — 0.73, p=0.008), which should protect the existing 3L+ accelerated approval. The optionality sits in LOTIS-7 — ZYNLONTA plus the bispecific glofitamab — which reported an 89.8% overall response rate (ORR) and 77.6% complete response (CR) rate in 49 evaluable r/r DLBCL patients. Management projects $600M–$1B U.S. peak revenue. At a ~$167M market cap, if the combination franchise is real, the equity is a multi-bagger off a busted-Phase-3 base.

The Bear Case. LOTIS-5 bought a 1.4-month median PFS improvement (6.1 vs 4.7 months) with a nearly tripled fatal-adverse-event rate: 27 Grade 5 deaths (13.2%) in the ZYNLONTA arm versus 9 (4.6%) in control. Overall survival (OS) was dead flat (HR 0.96, p=0.74). Worse, in patients ≥75 — 40% of the trial — there was no PFS benefit (HR 1.07) and an OS harm trend (HR 1.38). And the FDA just told the industry how it feels about exactly this setup: in May 2025 an ODAC panel voted 8–1 that glofitamab’s STARGLO trial — a stronger dataset in the same 2L r/r DLBCL population against the same R-GemOx control — was not applicable to U.S. patients, drawing a Complete Response Letter. LOTIS-5 enrolled just 6–8% North American patients and carries a fatal-tox signal STARGLO did not. Layer on ~$420M of debt-plus-royalty obligations against a $167M market cap, a 15.87% term loan, a live minimum-revenue covenant, and Redmile trimming into the crash, and the path to zero is not hard to draw.

Bottom Line. This is a busted growth story with a surviving base business and one genuinely interesting combination read still to come. The endpoint win likely defends the 3L+ label floor, but the 2L+ expansion — the reason to own this — now faces a brutal benefit-risk and regulatory gauntlet. Watch List, not investable here. The catalysts are dated and the valuation already reflects a lot of pain, but the balance sheet and the FDA math keep this off the buy sheet until LOTIS-7’s full data and the sBLA outcome resolve.

Catalyst Calendar & Financial Runway

Upcoming Catalysts (next 12–18 months):

August 2026 — FDA pre-sBLA meeting (LOTIS-5). A supplemental Biologics License Application (sBLA) is the filing to expand a marketed drug’s label. Not a public readout, but management has promised commentary; any leak that the FDA is lukewarm on the 2L+ benefit-risk is a de-facto catalyst.

Q4 2026 — LOTIS-5 sBLA submission for ZYNLONTA + rituximab in 2L+ r/r DLBCL.

Q4 2026 — LOTIS-7 full data (ZYNLONTA + glofitamab, N=100 dosed) at a medical meeting, plus regulatory/compendia pathway assessment. This is the real binary.

Q4 2026 — Marginal zone lymphoma (MZL) IIT data; Q2 2027 — follicular lymphoma (FL) IIT data (IIT = investigator-initiated trial, i.e., run by academic investigators rather than the company).

1H 2027 — potential compendia inclusion (LOTIS-5, LOTIS-7); 2H 2027 — potential confirmatory approval in 2L+ DLBCL.

The Dilution Gap.

Cash and equivalents were $231.0M at March 31, 2026, down from $261.3M at year-end 2025.

Operating cash burn was $29.7M in Q1 (much improved from $56.3M in Q1 2025 post-restructuring).

Management guides “cash runway at least into 2028” — but read the asterisk: that guidance assumes drawing down to the minimum liquidity the loan covenants require, i.e., $60M of cash that must be held at each quarter-end. So usable cash is closer to $231M − $60M ≈ $171M. Against ~$110–120M annualized burn (falling toward ~$100M after the reorg’s ~$10M savings), the runway “into 2028” is arithmetically fair but leaves nothing for the $99.8M term-loan balloon due in 2029. A raise is not needed before the next data drop — but with the stock at $1.31 and a 2029 maturity wall, dilution is a question of when, not if, and the equity has no leverage to wait for a good print.

Insiders & Institutions.

The anchor holder is Redmile Group at ~9.9% (~12.7M shares) — but Redmile sold ~5.88M shares in late March/early April 2026 at ~$3.28–$3.80, before the June collapse, trimming from a prior ~14%. That is either enviable timing or a conviction crack; either way it is not a vote of confidence.

Other holders: Prosight ~6.8% (adding), Point72 ~7.0%, OrbiMed ~5.9M shares, BlackRock ~5.0%, Nantahala ~5.5M (+142%).

Founding sponsor Auven exited years ago. On insiders, there is no open-market buying; the only notable recent grant was 675,000 RSUs to CEO Ameet Mallik on June 30, 2026 (comp, not conviction).

Post-data, sell-side cut hard: RBC downgraded to Sector Perform and slashed its target from $6 to $2; H.C. Wainwright went Buy→Neutral and pulled its target; Stephens held Overweight but cut $8→$5.

The Science: Mechanism & Chemistry

ZYNLONTA is a biologic — a humanized IgG1 anti-CD19 monoclonal antibody site-conjugated through a protease-cleavable valine-alanine linker to SG3199, a pyrrolobenzodiazepine (PBD) dimer, at a drug-antibody ratio of ~2.3. It is best classified as a best-in-class-payload ADC rather than a novel target: the target (CD19) is thoroughly de-risked; the warhead (PBD) is what differentiates — and what complicates.

Mechanism Validation. CD19 is arguably the most validated target in B-cell malignancy. It is hit by three approved CAR-Ts (axicabtagene ciloleucel/Yescarta, lisocabtagene maraleucel/Breyanzi, tisagenlecleucel/Kymriah), by the Fc-engineered naked antibody tafasitamab (Monjuvi), and by the CD19×CD3 bispecific blinatumomab (Blincyto). ZYNLONTA is the approved CD19 ADC. There is no “does the target work” question here — the question is whether this payload’s therapeutic index is wide enough for earlier lines.

Manufacturing / CMC Risks. ADC manufacturing is a three-way logistics problem — antibody, highly potent payload-linker, and conjugation/fill-finish — and ADCT runs it through a “top-tier external manufacturing network” of third-party CMOs. Highly potent PBD payloads require containment-grade handling; the company carries the usual biologic cold-chain and single-source exposures.

Biochemical Deep Dive

The Target. CD19 is a B-lymphocyte surface glycoprotein expressed from pro-B through mature B stages and retained on the majority of B-cell lymphomas, including essentially all DLBCL. Critically for an ADC, CD19 internalizes on antibody binding, delivering the conjugate into the lysosome. Because it is not shed and is near-ubiquitous on malignant B-cells, it tolerates the “one payload, many patients” ADC model — and, usefully, ZYNLONTA’s activity does not require high CD19 immunohistochemistry expression, so there is no companion-diagnostic gating [Source: LOTIS-2 subgroup analyses, Caimi et al., Lancet Oncol 2021].

The Chemistry. This is the differentiator and the liability in one molecule. Most approved lymphoma ADCs and their cousins carry microtubule inhibitors — polatuzumab vedotin and brentuximab use MMAE (auristatin); Enhertu uses a topoisomerase-I payload (DXd). ZYNLONTA instead delivers a PBD dimer, a DNA minor-groove interstrand cross-linking alkylator that, per the company’s own description, “binds to DNA minor groove with little distortion, remaining less visible to DNA repair mechanisms”. PBDs are picomolar-potent — far more cytotoxic than auristatins. That potency drives deep responses in chemo-refractory disease. It also drives a class-characteristic toxicity fingerprint: myelosuppression, hepatotoxicity (GGT elevation), and the AESI that should make every reader pause — edema/effusions, including pleural and pericardial effusions. PBD-warhead ADCs have a checkered safety history across the industry; the effusion/edema and hepatic signals in LOTIS-5 are the payload, not a fluke.

The Mechanism.

CD19 binding → endocytosis of the ADC-antigen complex → lysosomal degradation → protease cleavage of the valine-alanine linker → intracellular release of the PBD payload → covalent DNA interstrand cross-links → cell-cycle arrest → apoptosis, with a potential bystander effect on neighboring tumor cells.

The elegance is that DNA cross-links are agnostic to the proliferative rate and mutational escape routes that let lymphomas dodge microtubule poisons — which is why ZYNLONTA responds in double/triple-hit and primary-refractory disease.

The Biomarker Receipts. Here the honesty tax comes due: the translational package is thin relative to the mechanistic story. The strongest “receipt” that the mechanism operates in humans is the response itself — 48.3% ORR / 24.1% CR as 3L+ monotherapy in LOTIS-2, across CD19-expression strata. There is no rich pharmacodynamic biomarker cascade (no pSTAT, no serial cytokine kinetics) driving the thesis; efficacy and the PBD-class AE profile are the biomarkers. That is adequate for an approved drug but leaves little mechanistic cushion to argue the tox away.

Bottom Line for the thesis: the biology is sound and the payload is the edge — but the same PBD potency that generates CRs in refractory disease is what produced 27 fatal events in LOTIS-5. The therapeutic index, not the target, is the whole investment question.

Clinical Data

The setup.

LOTIS-5 (NCT04384484) is a randomized, open-label, two-arm, multicenter Phase 3: ZYNLONTA 150 µg/kg + rituximab for 2 cycles then ZYNLONTA 75 µg/kg + rituximab for up to 6 more, versus R-GemOx (rituximab-gemcitabine-oxaliplatin), in 2L+ transplant-ineligible r/r DLBCL.

N=420 randomized 1:1 (210/arm); treated population 401; data cut February 16, 2026.

Primary endpoint PFS by independent review committee (IRC); key secondary OS.

Efficacy.

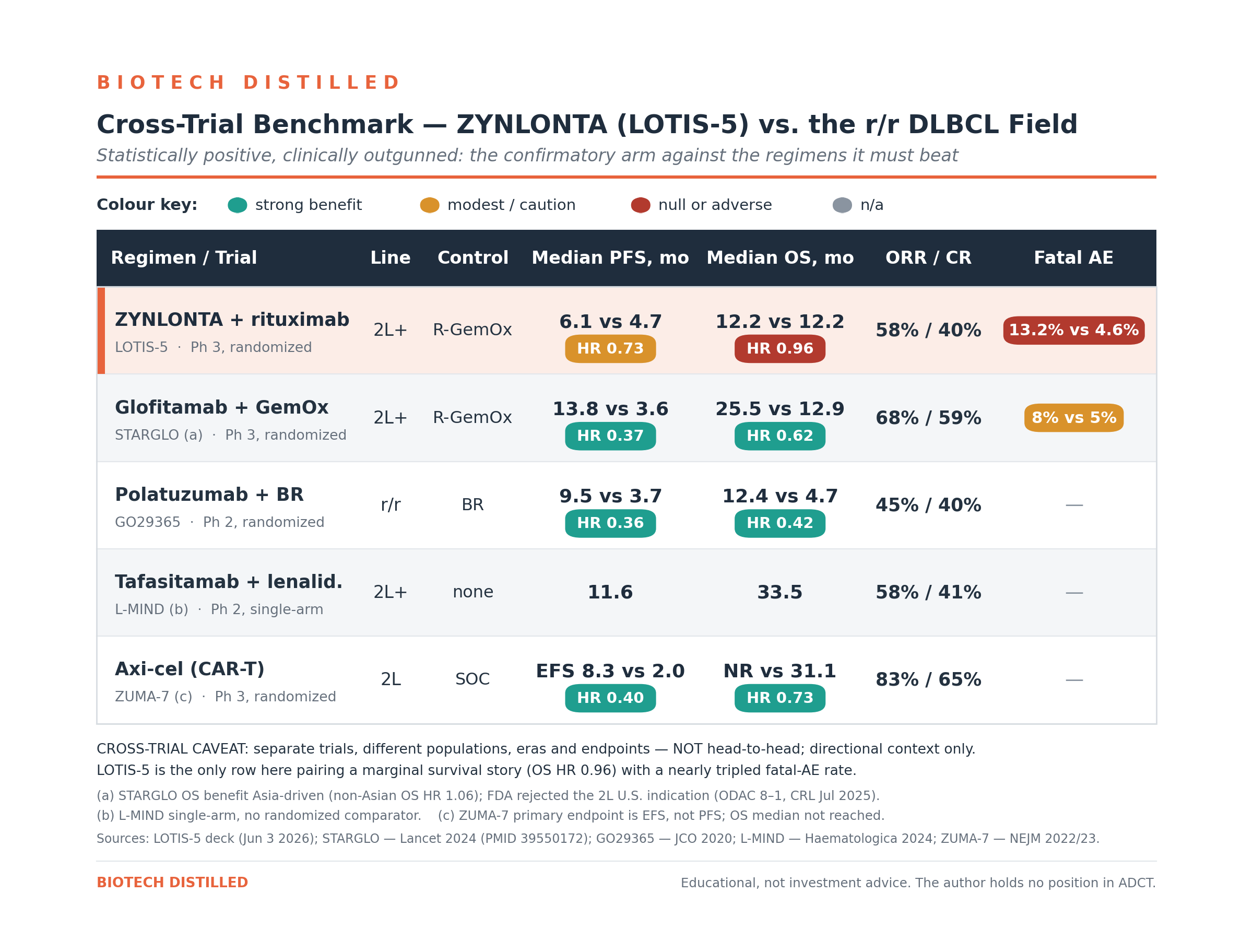

PFS met significance: median 6.14 vs 4.73 months, HR 0.73 (95% CI 0.57–0.92), two-sided p=0.0084.

Response rates favored ZYNLONTA: ORR 58.1% vs 45.2%, CR 39.5% vs 26.7%, with durable CRs (median duration of CR 16.8 vs 12.3 months; 48.5% vs 16.7% of complete responders still in CR at 24 months).

Those are real, and the CR durability is the best part of the story.

But overall survival was flat: median 12.19 vs 12.16 months, HR 0.96 (0.75–1.23), p=0.7387. Management leans on an IPCW (inverse-probability-of-censoring-weighting) sensitivity analysis adjusting for new anti-lymphoma therapy (HR 0.82) — but that is a post-hoc, model-based adjustment, not the pre-specified OS result. For a confirmatory trial meant to verify clinical benefit, a dead-flat OS is the number that matters.

Two reads jump out.

A historical R-GemOx benchmark runs ~3–5 months PFS / ~10–11 months OS (Mounier 2013; Cazelles 2021), so LOTIS-5’s control arm is normal, even slightly favorable — not a weak strawman. The modest delta is therefore about the experimental arm, not a rigged comparator.

And more damaging: STARGLO tested a better drug (glofitamab) against the identical R-GemOx control in the same population, produced vastly better PFS and OS, and the FDA still rejected it for the 2L U.S. indication (ODAC 8–1, May 20, 2025; CRL July 18, 2025) — largely because the OS benefit was Asia-driven (non-Asian OS HR 1.06) and U.S. enrollment was thin. LOTIS-5 enrolled just 6.2%/8.1% North American patients (≈30 patients total), carries weaker efficacy, and adds a fatal-tox signal. Management’s “results in North America were consistent with overall” is statistically hollow across ~30 patients — and it is precisely the vulnerability that sank a stronger competitor.

The P-Hacking / denominator checks.

The pre-specified OS is flat; the favorable OS number is the IPCW-adjusted one.

The ITT PFS win is carried entirely by younger patients: <75 years, PFS HR 0.55 and OS HR 0.72; ≥75 years, PFS HR 1.07 (no benefit) and OS HR 1.38 (harm trend) — and ≥75s were 40%+ of enrollment.

Management argues the higher AE rates partly reflect longer observation time in the ZYNLONTA arm (median TEAE follow-up 3.9 vs 2.5 months, because control patients switched to new therapy sooner) — a legitimate confounder for rates, but it cannot explain away 27 absolute Grade 5 deaths versus 9, most from on-treatment infections.

Safety — the quiet killers (this is the whole ballgame).

Overall Grade ≥3 TEAEs (treatment-emergent adverse events) were similar (74.0% vs 76.1%), and ZYNLONTA actually caused less hematologic toxicity than R-GemOx (40.7% vs 59.4%).

But the differentiating harms all point the wrong way: serious TEAEs 49.0% vs 34.5%; TEAEs leading to drug withdrawal 25.5% vs 9.1%; and Grade 5 (fatal) TEAEs 27 (13.2%) vs 9 (4.6%), with drug-related Grade 5 events 2.9% vs 1.0%.

The fatal events were dominated by infections (15 vs 5; pneumonia 9 vs 1, sepsis 3 vs 4) plus cardiac and general-deterioration events.

PBD-class AESIs (adverse events of special interest) were elevated as expected: hepatotoxicity Grade ≥3 17.2% vs 8.1%, edema/effusion 7.4% vs 0.5% (pleural effusion 5.4% vs 0).

And 59% of the ZYNLONTA-arm fatal events occurred in patients ≥75 — the same group getting no efficacy benefit.

Data Integrity. Randomized 1:1, multicenter, ITT primary analysis, IRC-adjudicated PFS — methodologically the endpoint is credible, and IRC (HR 0.73) was actually less favorable than investigator assessment (HR 0.65), which is reassuring. The weaknesses are open-label design (no blinding), a heavily non-U.S. and elderly population (median age 73; Europe 43%/34%, Asia 22%/21%, North America 6%/8%), and the fact that the drug’s benefit disappears in the 40% of patients who were ≥75.

Pipeline

Post-2025 restructuring, ADCT is effectively a one-drug company — every value driver below is ZYNLONTA in a different line or combination.

ZYNLONTA monotherapy — 3L+ r/r DLBCL (approved). Accelerated approval (FDA, April 2021); conditional approval (EU). ~$74M/yr, flat-to-slightly-up, price-driven, ~6,600-patient 3L+ addressable pool.

Reality check: this is the floor, and LOTIS-5’s positive PFS likely defends it as the confirmatory trial. Value driver — but a mature, low-growth one.

ZYNLONTA + rituximab — 2L+ r/r DLBCL (LOTIS-5, Phase 3). sBLA planned Q4 2026; management ascribes $200–300M of peak revenue to it].

Reality check: hit PFS, flat OS, fatal-tox signal, STARGLO precedent, 6–8% U.S. enrollment. The endpoint may protect the 3L+ label but the 2L+ approval is a coin-flip at best and, if approved, likely lands with a restrictive label and a tox warning. Impaired value driver.

ZYNLONTA + glofitamab — 2L+ DLBCL (LOTIS-7, Phase 1b). N=100 dosed at 150 µg/kg; prior cut 89.8% ORR / 77.6% CR in 49 evaluable patients; full data Q4 2026. Management ascribes $500–800M — the bulk of the $600M–$1B peak — to the bispecific combination.

Reality check: the single most important asset in the story and the real optionality — but it is Phase 1b, single-arm, N=49 on efficacy, layering ZYNLONTA’s infection/effusion tox onto glofitamab’s cytokine-release and infection risk (the protocol mandates anti-infective prophylaxis, IVIG, and vaccination — a tell). It will need its own randomized trial, and glofitamab’s own 2L combo was rejected in the U.S. Highest-upside, highest-variance. Optionality, not yet a value driver.

Indolent lymphoma IITs. ZYNLONTA monotherapy in r/r MZL (ORR ~85% / CR ~69%, N=26) and ZYNLONTA + rituximab in high-risk r/r FL (ORR ~98% / CR ~84%, N=55), investigator-initiated; data 2026–2027.

Reality check: eye-catching response rates but tiny, investigator-run, single-arm; a compendia/label path here is years and controlled trials away. Optionality.

Preclinical / solely-owned ADCs. The restructuring left an early PSMA-targeting ADC and exatecan-based conjugates (the solely-owned patent families expiring 2041–2046).

Reality check: zero-NPV placeholders at today’s cash position; platform credibility for an M&A story, not a model input.

Pipeline Verdict. ZYNLONTA carries 100% of the valuation. The 3L+ franchise is the floor; LOTIS-7 is the call option that matters; everything else is either impaired (LOTIS-5 2L+) or optionality (IITs, preclinical).

Intellectual Property & The Moat

The summary provided below is based on the 10-K filed by the Company in March 2026 and the 10-Q filed in May 2026.

ADCT reports over 230 patents issued across the U.S. and foreign jurisdictions (inclusive of counterparts), with expirations ranging 2031 to 2040, plus numerous pending applications. The estate splits into the in-licensed PBD-platform families, product families co-owned with MedImmune, and solely-owned families around newer warheads (exatecan) and linkers.

Asset-specific patent runway — ZYNLONTA. This is where the skeptic earns their keep: the loncastuximab antibody itself is reportedly “in the public domain” — there is no composition-of-matter wall around the naked antibody. Protection instead comes from six patent families directed to the ADC product, methods of use, and dosing regimens, co-owned with MedImmune, with issued/pending patents expiring 2033–2042. The regulatory backstops matter more than usual here: ZYNLONTA is a biologic with 12-year BPCIA reference-product exclusivity running from the April 2021 approval (to ~2033), plus 7-year orphan exclusivity. Net: an effective runway into the early-to-mid 2030s, leaning as much on BPCIA and method/dosing patents as on any single composition claim.

Ownership & licensing structure. The PBD warhead/linker is in-licensed — originally from Spirogen (2011), transferred to MedImmune/AstraZeneca after AZ acquired Spirogen — granting ADCT an exclusive worldwide license for PBD ADCs against up to 11 targets (CD19 included). The economics are unusually clean: a single $2.5M upfront paid in 2011 and, reportedly, no further royalties or milestones owed to AstraZeneca/MedImmune]. However, ADCT’s cost of product sales includes a royalty payable to a collaboration partner on ZYNLONTA net sales (historically the antibody-contributing partner; not named verbatim in the retrievable sections) — a separate skim on the top line to model.

The real “anti-moat” — the capital stack sits ahead of the equity. Two obligations claim ZYNLONTA’s cash flows before shareholders see a dollar:

HealthCare Royalty (HCRx) deferred royalty: ADCT sold 7% of worldwide ZYNLONTA net sales (stepping toward 10%) for $300M received; carrying value $304.7M; a 2.25x–2.5x cap ($675–750M). The February 2026 amendment cut the change-of-control payment from $675–750M to $150–200M and issued HCR 9.83M warrants at $3.81. That amendment is a tell — reducing the CoC toll makes the company materially easier to sell.

Oaktree / Blue Owl senior secured term loan: $120M drawn (of a $175M facility), carrying value $115.7M, effective interest rate 15.87%, maturing August 2029 with a $99.8M balloon. The covenants are the live risk: a $60M minimum-liquidity floor and a minimum U.S. ZYNLONTA revenue covenant that is active whenever the 30-day average market cap sits below $650M — which, at ~$167M today, it emphatically does. A sales stumble could trip a covenant into a distressed renegotiation.

Competitive Landscape. The 2L+ r/r DLBCL “shark tank” is crowded and moving toward T-cell engagers and CAR-T.

CAR-T (axi-cel, liso-cel) owns 2L for transplant-ineligible fit patients on the strength of a real OS win (ZUMA-7).

Bispecifics glofitamab (Columvi) and epcoritamab (Epkinly) are approved in 3L+ and pushing earlier.

Polatuzumab (Pola-BR/-R-CHP) and tafasitamab-lenalidomide occupy the antibody-combo niche ZYNLONTA is targeting.

ZYNLONTA’s differentiation is genuine — a chemo-free, outpatient-accessible, CD19 ADC that works in refractory/double-hit disease without CAR-T logistics — but the LOTIS-5 tox profile undercuts the “accessible and tolerable” pitch that was supposed to be its lane. Management sizes 2L+ DLBCL at ~$3B U.S. by 2030; independent estimates for the r/r DLBCL market are more like ~$2B by 2030 — either way, ZYNLONTA is fighting for a slice against better-validated mechanisms.

The Verdict

Scientific Conviction: Medium. The CD19 target and PBD payload are real and differentiated; LOTIS-5 confirmed PFS. But flat OS, a tripled fatal-AE rate, and zero benefit in the ≥75 subgroup cap the conviction.

Commercial Viability: Low-to-Medium. A ~$74M franchise that is genuinely defensible at 3L+, but the growth case (2L+ expansion, combos) is impaired and the capital stack skims the top line.

M&A Appeal: Medium. The paid-up PBD platform, a marketed product, and — tellingly — the February 2026 amendment that slashed the HCR change-of-control payment to $150–200M make ADCT easier to acquire. AstraZeneca (already the PBD licensor via MedImmune) is the logical strategic; a specialty/royalty buyer could want the cash-flowing 3L+ label. But an acquirer may simply wait for distress.

Trader Profile. Busted-Phase-3 special situation. For M&A specvestors and binary-event gamblers positioning into LOTIS-7 Q4 2026 — not for compounders, and not for anyone who needs a clean balance sheet.

The Buy (Speculative) Thesis.

Target Audience: deep-value / event-driven specvestors comfortable with binary risk and dilution.

Rationale: the stock has already de-rated ~57% from its ~$3.08 pre-topline close to ~$1.31 (with an intraday trough of $0.78 on June 8), to a ~$167M market cap [Source: stockanalysis.com]. LOTIS-5’s positive PFS plausibly defends the 3L+ label (a real ~$74M cash-flowing franchise), so this is not an empty shell. LOTIS-7’s 89.8% ORR / 77.6% CR combination is legitimately differentiated, reads out in full in Q4 2026, and the February 2026 HCR amendment quietly made the company far cheaper to buy. If LOTIS-7 holds and an ADC-hungry strategic (AstraZeneca is already the PBD licensor) steps in, this re-rates violently.

Execution/Strategy: consider sizing it as a lottery ticket, not a position — the balance sheet and covenant risk mean you can be right on the science and still get diluted. If you insist on shares, consider buying the drift ahead of Q4 data and plan to trim into any pop, because a “positive” ADCT headline has already proven it can still sell off.

The Hold Thesis.

Target Audience: existing holders underwater from the June collapse.

Rationale: the worst single-day repricing is behind you, the 3L+ floor and LOTIS-7 optionality are real, and forced-selling into a $0.78 low likely locks in the trough. But adding here means underwriting a leveraged, single-asset story into an FDA benefit-risk fight it might lose.

Execution/Strategy: consider holding a reduced core into the Q4 2026 LOTIS-7 readout and the sBLA outcome; think twice before adding until the 2029 maturity/dilution question has an answer. Consider treating any pre-catalyst rally as a chance to right-size, not to double down.

The Sell / Avoid Thesis.

Target Audience: quality-focused biotech investors and anyone who cannot model a covenant breach.

Rationale: flat OS, a tripled fatal-AE rate, no benefit in 40% of the trial, the STARGLO precedent, ~$420M of obligations against $167M of equity value, a 15.87% loan with a 2029 balloon, a live revenue covenant, no smart-money crossover funds, and Redmile trimming into strength. The “positive” Phase 3 was a value-destruction event for a reason.

Execution/Strategy: if you own it and the thesis was the 2L+ expansion, that thesis is impaired — consider selling into strength rather than hoping the FDA is generous.

Final Verdict

WATCH LIST. A real CD19 ADC with a confirmed-PFS 3L+ floor and a genuinely interesting bispecific combination (LOTIS-7) keep this from being a PASS — but flat OS, a fatal-tox signal, the STARGLO regulatory precedent, and a ~$420M capital stack against a $167M equity keep it firmly off the buy list until the Q4 2026 LOTIS-7 data and the sBLA path resolve.

This report is strictly for informational and educational purposes only. It does not constitute financial advice, investment advice, or a recommendation to buy or sell any securities mentioned.

The scientific and clinical analyses herein should not be interpreted as medical guidance, diagnostic information, or treatment recommendations.

At the time of writing, the author does not hold a position in ADC Therapeutics (ADCT).

Biotech investing is inherently volatile. Past scientific validation does not guarantee future clinical or regulatory success. Treat all clinical-stage biopharma allocations accordingly.

For informational and educational purposes only — not investment advice. The author's position (if any) is as stated in the original article. Always verify against primary sources and do your own due diligence.